From 1 July 2021, for-profit entities preparing financial statements in accordance with the Corporations Act 2001, other legislation, their constituting documents or other agreements will not be permitted to prepare Special Purpose Financial Statements (“SPFS”). At the same time, the existing Tier 2 Reduced Disclosure Regime (“RDR”) will be replaced by new Tier 2 disclosure requirements.

Removal of the ‘reporting entity’ concept

The Australian Accounting Standards Board (“AASB”) has now issued amendments that require, for annual reporting periods commencing from 1 July 2021, all for-profit entities that are required by legislation to prepare financial statements that comply with either ‘Australian Accounting Standards’ or ‘accounting standards’ to prepare General Purpose Financial Statements (“GPFS”).

This means that, unless an ASIC exemption exists, all for-profit companies such as large proprietary companies (including grandfathered or wholly-owned subsidiaries), unlisted public companies, foreign controlled small proprietary companies and financial services licensees preparing financial statements under the Corporations Act 2001 will have to prepare GPFS.

The requirement extends to the financial reporting obligations of other for-profit entities under Federal or State legislation such as indigenous corporations; incorporated associations; co-operatives; higher education providers; and residential aged care providers.

In addition, other for-profit private sector entities that are required by their constituting document or another document to prepare financial statements that comply with ‘Australian Accounting Standards’ will also have to prepare GPFS, if that document was created or amended on or after 1 July 2021. This has the potential to require entities that enter into new or amended borrowing agreements, constitutions, business acquisition agreements, or another agreement after 1 July 2021 that contains a requirement to prepare financial statements in accordance with Australian Accounting Standards to prepare GPFS.

What this means

- Entities in scope will have to comply with full recognition and measurement requirements of Australian Accounting Standards. The main potential effects for entities that have not applied all recognition and measurements requirements in the past are likely to be the adoption of:

- Business Combinations (AASB 3)

- Consolidation (AASB 10)

- Equity accounting (AASB 128)

- Leases (AASB 16)

- Financial Instruments (AASB 9)

- Revenue (AASB 15)

- Fair Value Measurement (AASB 13)

- For-profit entities not in scope of the new requirements, for example small proprietary companies and trusts, can still prepare SPFS provided there is no other document that requires the preparation of GPFS and there are no users dependent on GPFS to meet their information needs.

- These changes do not apply to not-for-profit (“NFP”) entities. However, the AASB is intending to extend these requirements to NFP entities in the future.

Composition of Tier 2 GPFS

The second part of the AASB’s changes is to replace the existing Tier 2 RDR (Reduced Disclosure Regime) GPFS standard with a new disclosure standard called ‘Simplified Disclosures for Tier 2 Entities’ (“SDS”).

The new Tier 2 SDS will apply to for-profit and not-for-profit entities preparing Tier 2 GPFS. The replacement of the existing RDR by the SDS standard will also be mandatory for reporting periods beginning on or after 1 July 2021, although early adoption is permitted.

The SDS disclosures are somewhat less than the existing RDR disclosures. Because many entities currently preparing SPFS do not comply with many disclosure requirements in accounting standards, it is likely that financial report disclosures will increase under SDS compared to their existing SPFS.

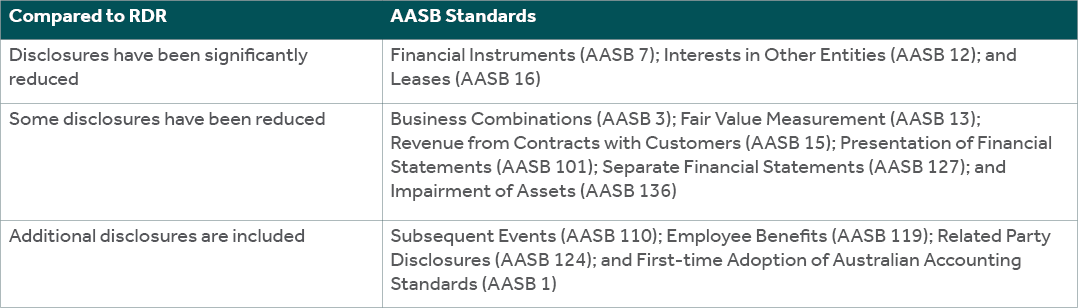

The following is a summary of the main differences between RDR and SDS:

There are no significant differences between the disclosure requirements of RDR and SDS in relation to other accounting standards.

What this means

- For those entities currently preparing Tier 2 RDR, whether a for-profit or NFP entity, there will be some reduction in disclosures.

- For those for-profit entities currently preparing SPFS, there are likely to be additional disclosures required in a number of areas, including related party disclosures and financial instruments.

Transition

Transition relief is available for entities that choose to early adopt before 1 July 2021 (eg, for 30 June 2020 or 30 June 2021 balance dates) and move from SPFS to Tier 2 SDS. This relief allows an entity not to restate comparative financial information, which will be presented in accordance with the entity’s previous accounting policies.

However, entities that do not early adopt and wait until 1 July 2021 will not receive any special transition relief and will have to restate comparative financial information in their first year of adoption. Hence, an entity first applying the new requirements in its 30 June 2022 financial statements will be required to restate its 2021 comparatives. However, if the entity first applies the new requirements in its 30 June 2021 financial statements it will not be required to restate its 2020 comparatives.

Will you be affected?

From 1 July 2021, for-profit entities that are required to prepare financial statements in accordance with Australian Accounting Standards and previously preparing SPFS are likely to face measurement, recognition and disclosure changes to their financial statements.

Affected entities should develop an action plan to:

- review their existing accounting policies and identify those areas of change, including the identification of any controlled entities;

- decide whether to early adopt the new requirements to financial years commencing before 1 July 2021;

- consider whether any changes are needed to internal systems and processes to enable consolidation of controlled entities and to capture information in respect of the new disclosure requirements.

If you require assistance preparing for these changes, including impact assessments and diagnostics, please contact your local Nexia Advisor.