Welcome to the newest edition of our Not-for-Profit Newsletter. Please feel free to contact us if you have any questions about the content of this Newsletter.

In this edition

With the 2023/24 financial year reporting season upon us, this edition includes important information on financial reporting updates and new requirements. Following on from previous editions that covered cyber-security matters, this edition includes information about a recent publication that provides guidance to assist NFPs strengthen their cybersecurity resilience. This edition also covers a number of governance and compliance matters, and ACNC activities.

Click on one of the Newsletter sections below to Scroll to the Section

| Governance | Cyber Security |

| Compliance | Financial Reporting |

| ACNC Activities | NDIS |

| Fraud |

Governance principles updated

The Australian Institute of Company Directors has released the third edition of its Not-for-Profit Governance Principles. The updated guidance reflects the demands of a changing governance environment since the 2019 edition.

Ten principles have become eight, new principles on sustainability and organisational culture published. How to elevate client voices into board decision-making is discussed.

The principles are:

- Principle 1 – Purpose, vision, and strategy

- Principle 2 – Roles and responsibilities

- Principle 3 – Board composition and effectiveness

- Principle 4 – Risk management

- Principle 5 – Performance and accountability

- Principle 6 – Stakeholders

- Principle 7 – Sustainability, and

- Principle 8 – Organisational culture.

Their guidance is grounded in director expertise, regulatory best-practice, and real-life case studies. A concise small NFP-governance checklist is included, as well as a brief snapshot of the overall principles. A governance checklist for smaller NFPs is featured.

AICD CEO and managing director Mark Rigotti said, ‘[The] NFP sector has experienced significant regulatory reform and disruption as well as an increase in community expectations.

‘This has arisen, in part, from a series of royal commissions, the COVID-19 pandemic, and emerging risks such as cyber and climate.’

Each NFP board should carefully consider how to apply the principles, Mr Rigotti added.

Directors convicted for failing to have DINs

Two Western Australian directors have been convicted and fined $5000 each for failing to comply with director-identification requirements.

Alexander Henry was convicted ex-parte for contravening section 1272C(2) of the Corporations Act 2001 for failing to have a director identification number. Mr Henry is a director of Global Material Solutions Australia Pty Ltd, Alex Henry Holdings Pty Ltd, Duke Shipping Containers Pty Ltd, and AII Australia Pty Ltd.

Luke David Mason was also convicted ex-parte of the same offence. Mr Mason is a director of LDM (WA) Pty Ltd, and LDM Corporate Enterprises Pty Ltd.

Magistrate Catherine Crawford said that new director IDs had been enacted for a proper public purpose and considerable efforts had been made by relevant government agencies to bring the accuseds’ attention to the scheme and obtain compliance.

Mr Henry and Mr Mason were each fined $5000 plus costs of $171.71. The maximum penalty for an offence against section 1272C(1) of the act is sixty penalty units or $18,780.

The maximum penalty for an offence against section 1272C(1) of the act is 60 penalty units. The defendant in this matter is facing a maximum fine of $13,320.

New resources on AI

As more organisations adopt artificial-intelligence technologies and policymakers focus increasingly on regulating AI risks, the need for directors and boards to understand governance requirements of ethical and informed AI use is rapidly becoming an imperative.

AI has the potential to offer significant productivity and economic gains. But alongside the benefits lie potential risks.

Research suggests that boards face many challenges, including how to implement effective surveillance systems.

The AICD has partnered with the Human Technology Institute at the University of Technology Sydney to produce a new suite of resources to help directors and boards navigate AI.

It contains:

- A Director’s Introduction to AI, which lays the foundations for understanding AI concepts

- A Director’ Guide to AI Governance, providing practical guidance for boards already using or planning to deploy AI within their organisations, and

- AI Governance Checklist SME and NFP Directors, which recognises the significance of small and medium-sized enterprises to the Australian economy and their specific needs.

By applying the ‘eight elements of safe and responsible AI governance’, the resources aim to guide organisations in deploying AI systems safely and responsibly and help them to optimise their strategic and competitive advantage.

Productivity Commission reports on philanthropic giving

The federal government has released the Productivity Commission’s once in a generation review of philanthropic giving. The review aims to boost donations to charities to help achieve a government target of doubling philanthropic giving by 2030.

Philanthropic giving underpins the crucial efforts of charities, NFPs, and community groups to support vulnerable Australians and better connect Australian communities.

The review recommends reforms to strengthen the foundations of philanthropy in Australia and increase giving.

Among nine significant findings is that the value of individuals’ tax deductible donations is increasing but fewer people are donating. A sound regulatory framework with greater transparency and consistency is important for supporting donors, it recommends.

The review sets out a range of proposals for short and long term reform that the government will consider.

Recommended changes to tax settings for donations to school building funds are not being considered.

The commission has made nineteen final recommendations focusing on four main areas:

- Improving the system that determines which charities have access to tax deductible donations

- Improving access to philanthropic networks for Aboriginal and Torres Strait Islander people

- Enhancing the regulatory framework for charities and ancillary funds, and

- Improving public information on charities and donations.

SMEs and NFPs get help on cyber security

The AICD and the Australian Information Security Association have released new guidance for small business and NFP directors to help them to strengthen their organisations’ cyber resilience.

The Cyber Security Handbook for Small Business and Not-for-Profit Directors aims to avoid unnecessary complexity.

The guide applies across the SME-NFP landscape, not just to organisations involved in digital and technology-focused industries.

It covers:

- The role of a director in an elevated cyber-threat environment

- The fundamentals of cyber security, and

- How to develop internal policies and build a culture of cyber resilience.

The guide is intended to complement the detailed Australian Signals Directorate’s Essential Eight maturity model and other key cyber-security guidance.

Minimum wages increase

The Fair Work Commission has announced a 3.75 per cent increase to the National Minimum Wage and minimum award wages.

From 1 July:

- The National Minimum Wage increases to $915.90 per week or $24.10 per hour, and

- Award minimum wages increase by 3.75 per cent.

Other award wages, including junior, apprentice, and supported wages that are based on adult minimum wages will get proportionate increases.

The increase applies from the first full pay period on or after 1 July 2024.

Changes in ATO reporting for NFPs

If a not-for-profit has an active Australian business number, it will need to lodge an NFP self-review return to access income tax exemption. Lodgements must be made from the 2023–24 income year onward.

Exempt are:

- A government entity or a charity registered with the Australian Charities and Not-for-profits Commission. Charities already lodge an annual information statement to the ACNC each year, and

- Similarly taxable not-for-profits, as they already lodge an income tax return.

Income-tax exempt entities that can self-assess their eligibility fall into eight categories: community service, sporting, cultural, educational, health, employment, scientific, and resource development.

NFPs must meet specific criteria and conditions to be eligible to self-assess as income-tax exempt. NFPs need to consider their purposes and activities against the criteria when completing an annual self-review.

Self-reviewed returns for the 2023–24 financial year may be lodged up to 31 October. They may be submitted online through Online services for business or a registered tax agent using Online services for agents.

World Vision Australia back-pays staff $6 million

World Vision Australia Pty Ltd has back-paid staff more than $6 million, including interest and superannuation, and has signed an enforceable undertaking with the Fair Work Ombudsman.

The charity self-reported underpayments to the FWO in December 2019 after an internal review identified compliance issues.

Non-compliance resulted in the underpayment of employees’ minimum wages, penalty rates and overtime, leave entitlements, and allowances.

World Vision Australia underpaid more than three thousand current and former employees over $4.6 million in wages and entitlements, which has been back-paid.

More than $1.4 million in superannuation and interest has also been back-paid.

Underpaid employees worked in every state and territory except for the Northern Territory, the majority based in Victoria and New South Wales. Both salaried and casual employees were underpaid.

Individual back-payments ranged from less than $50 to $84,394. The average back-payment was about $1900, including superannuation and interest,

Fair Work Ombudsman Anna Booth said an EU was appropriate as World Vision Australia had cooperated with the FWO’s investigation and demonstrated a strong commitment to rectifying underpayments and making changes to ensure future compliance.

‘Under the enforceable undertaking, World Vision Australia has committed to implementing stringent measures to ensure [that] all its workers are paid correctly. These measures include implementing a new time and wages payroll system and commissioning, at its own cost, at least one annual audit to check [to see that] it is meeting all employee entitlements’, Ms Booth said.

The EU also requires World Vision Australia to provide a report to the FWO on its progress in implementing improvements to its payroll and corporate governance systems, run for three months an independent employee hotline to take any workplace relations queries, and publish and display notices about the EU and its contraventions on its website and in its offices in Melbourne and Sydney.

Open Minds back-pays $4.2 million

Disability-support charity Open Minds Australia Ltd has back-paid staff about $4.2 million after breaching its own collective agreement and has signed an enforceable undertaking with the FWO.

The in-home care-and-support-services charity assists people with cognitive and physical disabilities across thirty-five sites in Queensland and northern NSW. In 2021, Open Minds became a subsidiary of Multicap Ltd.

Open Minds self-reported underpayments to the FWO in June 2021 having become aware of compliance issues after an internal payroll review found it had breached certain provisions of its collective agreement.

The charity was uncertain about the interpretation of its collective agreement and made errors in its payroll and rostering system, resulting in underpaid entitlements to do with sleepovers, penalty rates, overtime, allowances, and pay-point increments.

It resulted in 1507 current and former employees being underpaid $3.33 million, including more than $190,000 in superannuation, between July 2015 and July 2021. Open Minds has also back-paid more than $170,000 in interest.

In addition, Open Minds has back-paid about $695,000, including superannuation, to current and former employees after a review to ensure that the salaries paid under common-law contracts between 2015 and 2022 were above comparable collective-agreement entitlements.

Employees affected by the breaches were full-time, part-time, and casual support workers, residential support workers and case workers. Individual back-payments to employees ranged from small amounts to almost $50,000, and the average back-payment was about $2400, including superannuation and interest.

Fair Work Ombudsman Anna Booth said an EU was appropriate as Open Minds had cooperated with the FWO’s investigation and demonstrated a strong commitment to both rectifying underpayments and making changes to ensure that they were not repeated.

‘Under the enforceable undertaking, Open Minds has committed to implementing stringent measures to ensure all its workers are paid correctly. These measures include commissioning, at its own cost, an independent auditor to check it is appropriately meeting all employee entitlements’, Ms Booth said.

It was a wake-up call to employers to ensure that they understood and had systems that could correctly apply the terms of their own enterprise agreements.

‘Employers need to place a much higher priority on [ensuring] that […] employees’ full lawful entitlements are met, year-in, year-out’, she said.

The EU also requires Open Minds to provide a report to the FWO on its progress in implementing a new integrated rostering and payroll system, convene a payroll remediation committee, run an independent employee hotline for three months to take workplace queries, and write to underpaid staff to notify them that the EU had begun.

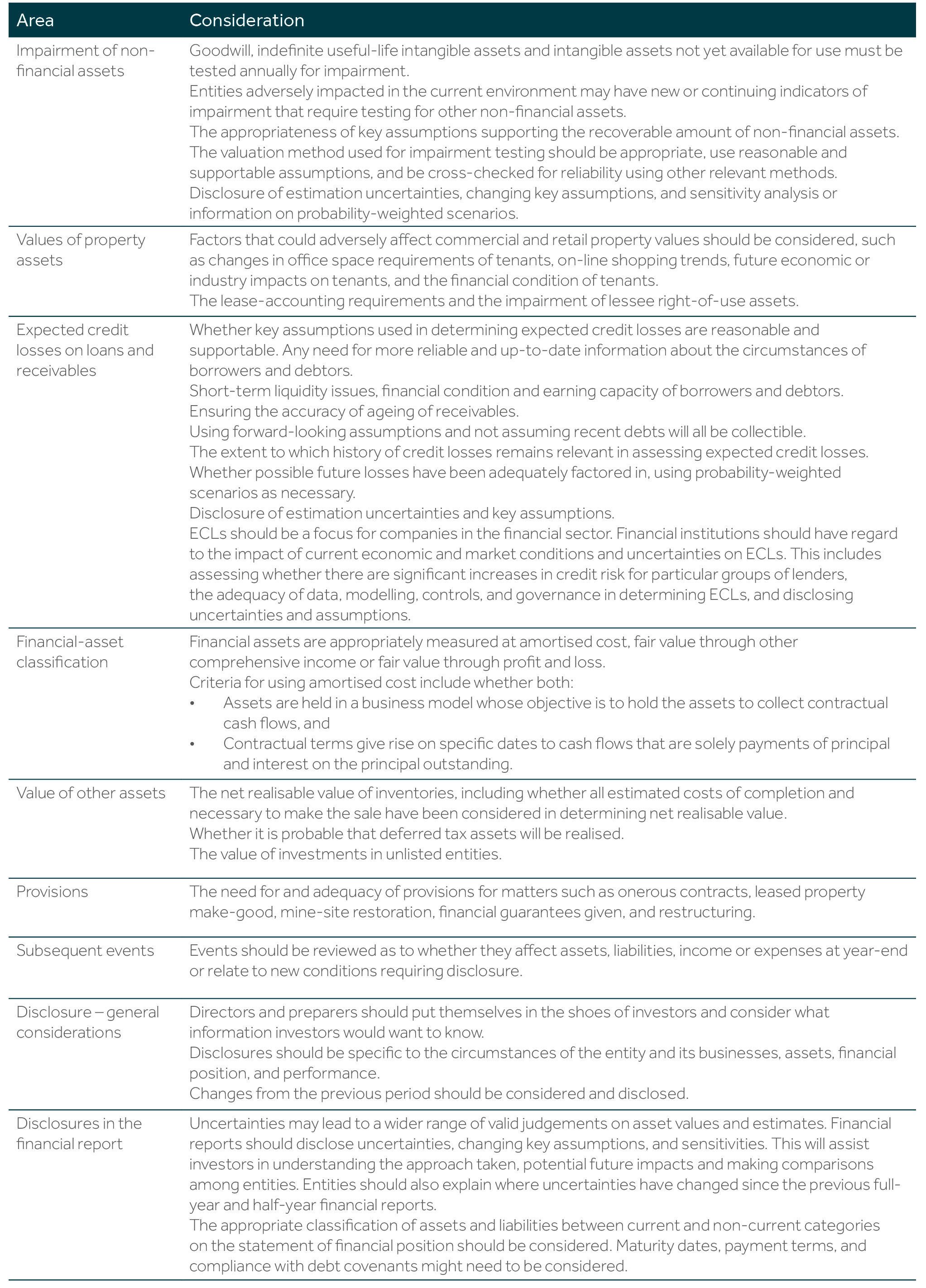

ASIC’s financial reporting focus

The Australian Securities & Investments Commission targets its surveillance of auditing and reporting in two tranches.

The first is what it calls ‘enduring’ areas. They apply to every reporting period and include asset values, adequacy of provisions, subsequent events, and disclosures. See table below ASIC ‘enduring’ focus areas for financial reporting.

In certain periods, these areas are supplemented by extra targets, depending on new regulatory requirements and emerging issues. These include climate change, consolidated entity disclosure statements, grandfathered entities, and registrable superannuation entities.

Directors are encouraged to engage closely with the federal government’s proposed mandatory climate-reporting reforms for entities that are required to prepare financial reports under Chapter 2M of the Corporations Act.

‘Directors need to be aware of the impending developments in climate-reporting’, said commissioner Kate O’Rourke.

‘The first tier of companies is proposed to report for financial years commencing from 1 January 2025. Directors and entities should start preparing and putting into place the necessary governance arrangements. They should consider what capabilities and data requirements may be needed.’

Entities with material climate-related risks should look to report voluntarily in line with recommendations of the Taskforce on Climate-related Financial Disclosures and ensure that any voluntary statements fail to mislead.

ASIC is continuing to monitor market practice on voluntary climate-related financial disclosures that will inform future compliance programs and guidance.

Large proprietary companies that had been previously ‘grandfathered’ are required to lodge financial reports for years ending on or after 10 August 2022. They are included in ASIC’s financial-reporting and audit-surveillance program.

Ms O’Rourke said, ‘We expect preparers, directors and auditors to pay particular attention to these focus areas in a collective effort to improve financial reporting and audit quality. ASIC will continue to focus on the financial-reporting elements that require the most judgement and make the most use of estimates.’

The commission will review the full-year financial reports of selected listed entities and other public-interest entities. This includes a sample of financial reports from the group of large proprietary companies that were formerly exempt from lodging audited financial statements with ASIC (grandfathered companies) but are now required to lodge, and registerable superannuation funds.

ASIC ‘enduring’ focus areas for financial reporting*

* Adapted for NFP reporting

ASIC’s crucial reminder

ASIC has reminded directors that they are primarily responsible for the quality of financial reports.

Responsibility includes ensuring that management produces quality and timely financial information for audit supported by robust position papers with appropriate analyses and conclusions referencing relevant accounting standards.

Companies must have appropriate processes, records, and analysis to support information in the report, the commission says.

Appropriate experience and expertise should be applied in reporting and auditing, particularly in more difficult and complex areas, such as asset values, provisions, and other estimates.

The circumstances in which judgements on accounting estimates and forward-looking information have been made and the basis for those judgements should be properly documented at the time and disclosed as appropriate.

Audit fees should be reasonable and relate to increased costs for auditors and additional effort required in judgement areas.

Material accounting policy information required

Under amendments to AASB 101 Presentation of Financial Statements disclosure is now required for material accounting-policy information – superseding disclosure of significant accounting policies.

Subtle but significant, the change These amendments apply to 30 June for the first time.

Accounting-policy information is material if, when considered together with other information included in an entity’s financial statements, it can reasonably be expected to influence decisions that the primary users of general-purpose financial statements make.

Accounting-policy information is expected to be material if users of an entity’s financial statements would need it to understand other material information in the statements.

Accounting-policy information is likely to be material if it relates to material transactions, other events or conditions, and:

- The entity changed its accounting policy during the reporting period, resulting in a material change to the information in the financial statements

- The entity chose the accounting policy from one or more options permitted by Australian accounting standards (and there are many)

- The accounting policy was developed in accordance with AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors in the absence of a standard that specifically applies

- The accounting policy relates to an area for which an entity is required to make significant judgements or assumptions, and the entity discloses them as required by AASB 101, and

- The accounting required for them is complex and statement users would otherwise fail to understand material transactions and other events or conditions.

Accounting-policy information that focuses on how an entity has applied accounting standards’ demands to its own circumstances provides entity-specific information that is more useful to statement users than standardised information or information that only duplicates or summarises standards’ requirements.

Accounting-policy information that relates to immaterial transactions and other events or conditions is immaterial and need not be disclosed.

The amendments aim to remove boilerplate accounting policies – often a summary of what an accounting standard requires. More information about entity specific judgements and estimates should result.

New ‘Consolidated Entity Disclosure Statement’

Among annual financial-reporting obligations under chapter 2M of the Corporations Act, Australian public companies (which can include NFPs but not those registered with the ACNC) must include from 1 July last year a ‘consolidated entity disclosure statement’.

The Treasury Laws Amendment (Making Multinationals Pay Their Fair Share – Integrity and Transparency) Act 2024 amends the Corporations Act 2001 to introduce the statement, which aims to enhance transparency around the tax residency of entities within a consolidated group.

The statement requires the following disclosures for each entity that was, at the end of the financial year, part of the consolidated group:

- The entity’s name

- Whether the entity is a body corporate, partnership, or trust

- Whether the entity was a trustee of a trust within the consolidated entity, a partner in a partnership within the consolidated entity, or a participant in a joint venture within the consolidated entity

- Where the entity was incorporated or formed (if the entity is a body corporate)

- Where the entity is a body corporate with share capital and the percentage of the entity’s issued share capital held directly or indirectly by the public company

- Whether the entity was an Australian resident or a foreign resident within the meaning of the Income Tax Assessment Act 1997, and

- If the entity was a foreign resident, a list of each foreign jurisdictions in which the entity was a resident for the purposes of the laws of the foreign jurisdiction.

The existing directors’ declaration will include a statement about whether, in the directors’ opinion, the ‘consolidated entity disclosure statement’ is true and correct.

ASIC’s information sheet 284 Consolidated Entity Disclosure Statement provides guidance to ensure that CEDSs comply with the requirements of the Corporations Act 2001 and is consistent with the policy intent of the legislation.

The sheet:

- Provides guidance on current developments, and

- Outlines what public companies need to be aware of when preparing their consolidated entity disclosure statements – reporting requirements, tax residence, true and correct, materiality, and audit and assurance.

A CEDS is subject to audit. The Auditing and Assurance Standards Board has issued a bulletin Audit Implications of the Consolidated Entity Disclosure Statement.

Finer profit-loss details required

The Australian Accounting Standards Board has issued AASB 18 Presentation and Disclosure in Financial Statements to improve how entities reveal their details, a particular focus being on information about performance in profit or loss.

AASB 18 will replace AASB 101 Presentation of Financial Statements. AASB18 makes consequential amendments to most of the AASB pronouncements.

The new requirements will enable investors and other statement users to make more informed decisions, including better capital allocation, which will contribute to long-term financial stability.

Key presentation and disclosure requirements are:

- Newly defined subtotals in the statement of profit or loss

- Management-defined performance measures, and

- Enhanced requirements for grouping information (that is, aggregation and disaggregation).

For for-profit entities (other than superannuation entities applying AASB 1056 Superannuation Entities) preparing Tier 1 general-purpose financial statements, AASB 18 applies to annual reporting periods beginning on or after 1 January 2027, earlier application permitted.

For not-for-profit private-sector entities, not-for-profit public-sector entities and superannuation entities applying AASB 1056, AASB 18 applies to annual reporting periods beginning on or after 1 January 2028, earlier application permitted. The delayed date will allow the AASB to consult with stakeholders to assess whether AASB 18 should be amended.

Latest insights on charity sector

The Australian Charities and Not-for-profits Commission has released the 10th edition of its Australian Charities Report, which details how cost-of-living pressures have affected charities.

While total sector revenue rose by $11 billion (or 5.6 per cent) to a record high of just over $200 billion in the 2022 reporting period compared with the year before, an increase in expenses of $22 billion (12.6 per cent) outstripped growth.

Employee expenses rose by nearly 10 per cent – the highest annual rise ever recorded.

The sector remains a major employer, accounting for 10.5 per cent of the Australian workforce. It continued to depend on volunteers, more than half of all charities operating with no paid staff. Volunteer numbers increased to 3.5 million – up from 3.2 million in the previous period.

Commissioner Sue Woodward said, ‘this comprehensive analysis helps us understand some of the challenges affecting charity operations’.

She added, ‘Our latest data demonstrates charities make an enormous contribution to Australia’s social fabric, its economy, and employment. It is important to recognise that the rise in expenses and liabilities outpaced the rise in revenue and assets in percentage terms’.

Donations to charities grew by 4.4 per cent. Donations and bequests totalled $13.9 billion, a rise of more than $584 million. Charities distributed $11.7 billion in grants and donations to other charities and not-for-profit organisations, mainly in Australia.

The 10th edition includes a spotlight on extra-small charities – those with annual revenue of less than $50,000. Accounting for about 31 per cent of the sector, they operate with just 0.1 per cent of its revenue.

In contrast, extra-large charities – those with $100 million or more in annual revenue – comprise 0.5 per cent of the sector but operate with more than 54 per cent of the revenue.

A five-year analysis comparing data from 2017 and 2022 reporting periods shows that almost 90 per cent of extra-small charities operated with no paid staff. Further, they had a 17 per cent drop in the number of volunteers and an 18 per cent drop in paid staff.

‘The differences between the smallest and largest charities could not be starker’, Ms Woodward said.

‘This five-year […] data shows the cost of operating and delivering services has increased but extra-small charities haven’t received sufficient revenue or donations to keep pace.’

Review of 2022 charities financial information

Aiming to improve the quality of data on the charity register, and compliance with reporting obligations, the commission reviews each year 250 annual information statements and financial reports.

The commission sought answers to the following:

- Did large charities comply with the key management personnel remuneration AIS reporting requirements?

- Were there material discrepancies when the financial information in the AIS was compared to AFR?

- Did the AFR include a complete set of financial statements?

- Did the AFR include a signed audit/review report and assigned responsible people’s declaration?

- Did the AFR include appropriate disclosure notes related to Related Party Transactions in compliance with AASB 124 Related Party Disclosures (or AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities)?

Key findings were:

- KMP remuneration reporting requirements: 28 per cent of charities made a material error when providing KMP information in AISs. Common errors occurred when charities stated that they had no more than one remunerated KMP in the AIS when the AFR showed otherwise and entered the total KMP remuneration figure incorrectly in the AIS

- Complete financial statements: 76 per cent of AFRs included a complete set of financial statements, major omissions being a statement of other comprehensive income – 22 per cent – and statement of cash flows 9 per cent

- Material discrepancies between the AIS and AFR: 91 per cent of charities reviewed did not have any material discrepancy when the commission compared key financial figures in AISs and AFRs. Material errors were most commonly due to incorrect reporting of ‘employee expenses’, and

- Ninety-five per cent attached a responsible people’s declaration to the AFR: 95 per cent of these were signed and dated. Ninety-seven per cent of declarations reviewed included a solvency statement, and 64 per cent of charities correctly selected the type of financial statements they prepared in their AIS. The most common error identified involved charities that usually prepared special-purpose statements incorrectly selecting general-purpose counterparts.

In addition to key management-personnel remuneration reporting, AASB 124 Related Party Disclosures and AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities require disclosures about other related-party transactions. Charities using GPFS-SDR had the highest compliance – 98 per cent provided general related-party transaction disclosures and 97 per cent included detailed disclosures.

Seventeen per cent of charities using SPFSs voluntarily provided general related-party transaction disclosures; 12 per cent included a detailed disclosure.

Audit and review reports showed that:

- Ninety-four per cent of AFRs included the auditor or reviewer report; of these, 97 per cent were signed and dated

- Seven per cent of auditor/reviewer reports had a modified opinion/conclusion, primarily in relation to cash donations, and

- Thirty-two per cent of auditor/reviewer reports had an ‘emphasis of matter’. Of those charities with an emphasis-of-matter paragraph, only 8 per cent were about going concern.

New charity-registration tool

The ACNC has launched an online, interactive tool to help organisations in assessing their eligibility to be registered as a charity and help those already registered to check their ongoing entitlement.

The new Charity Registration Check asks specific questions about an organisation’s circumstances and provides tailored responses. Based on the responses, the tool outlines the next steps that need to be taken, helping users understand charity-registration criteria and the information they need to provide to make a successful registration application or to maintain eligibility to be registered.

New applicants can use the tool to identify potential issues before submitting a formal registration application to the ACNC, while registered charities can use it to check that they are continuing to meet the requirements of registration, such as keeping responsible people’s names up-to-date.

Additionally, when the commission conducts annual reviews of deductible-gift-recipient eligibility, registered charities may be asked to use the tool to self-assess ongoing entitlement.

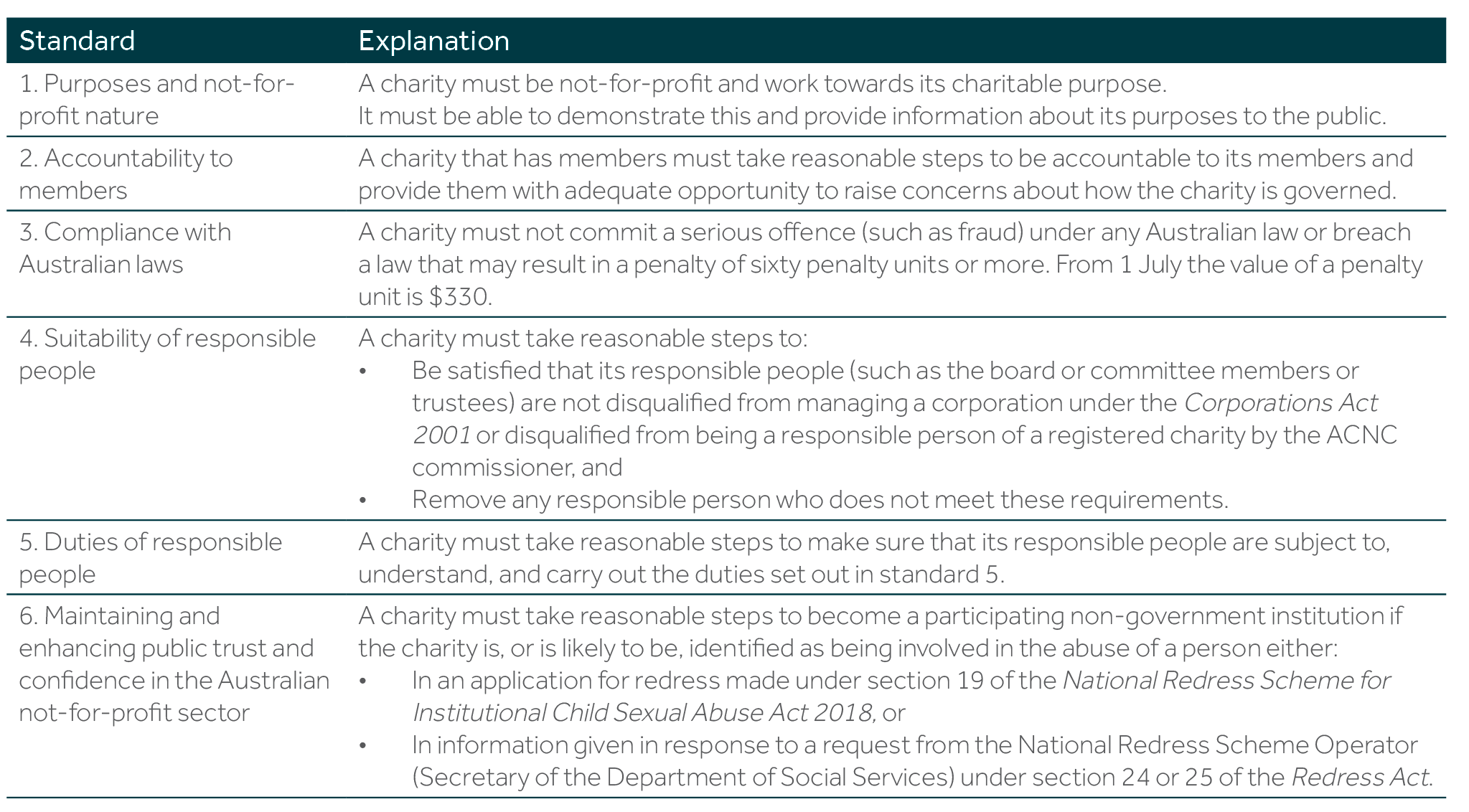

Adhering to ACNC’s governance standards

The ACNC’s governance standards is a set of core principles dealing with how a charity should be run.

Charities must meet the standards to be registered and remain registered. The principles do not apply to basic religious charities.

They require charities to remain charitable, operate lawfully, and be run in an accountable and responsible way. They help to maintain public trust in their work.

The principles are high-level, imprecise rules, and charities must determine what they need to do to comply with them.

An ACNC self-evaluation tool aims to help charities assess if they are meeting their obligations. It also helps to identify issues that might prevent them from doing so.

It poses questions and prompts charities to describe both the practical steps they are taking to meet their obligations and to list relevant policies or procedures.

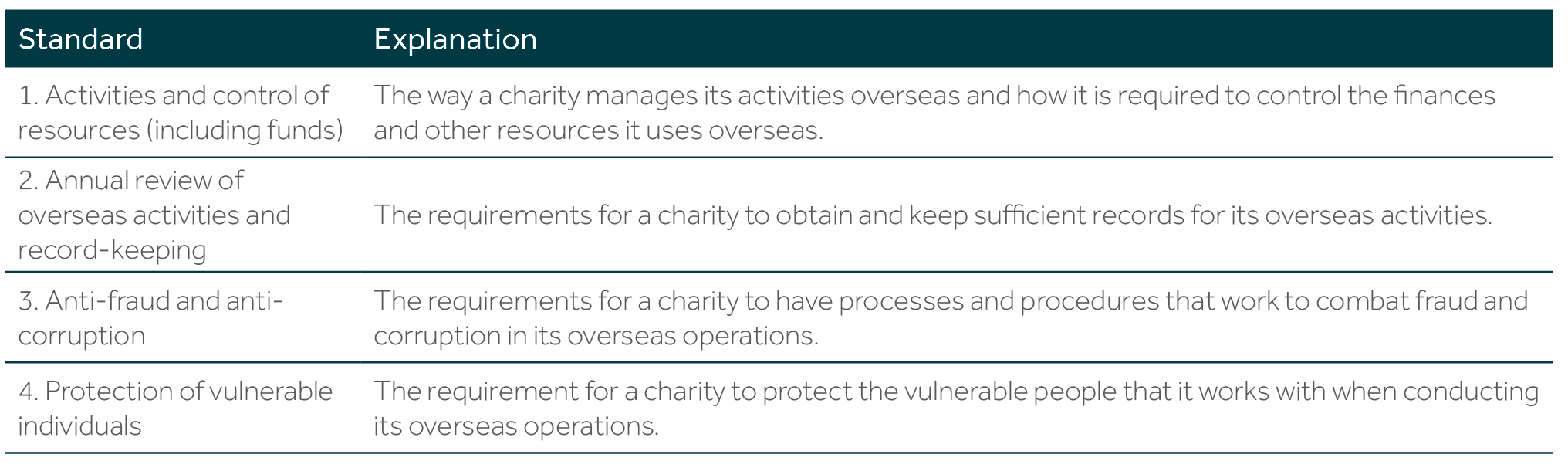

A charity that conducts activities overseas – including sending funds overseas from Australia – must also comply with external-conduct and governance standards.

Four external-conduct standards cover certain aspects of a charity’s overseas operations.

An ACNC self-evaluation tool for charities operating overseas aims to help charities assess if they are meeting their obligations and identify issues that might prevent them from doing so.

The tool poses questions and prompts charities to describe the practical steps they are taking to meet their obligations.

Disability provider fined almost $2 million

Disability support provider LiveBetter Services Ltd has been fined almost $2 million over the death of a National Disability Insurance Scheme participant.

Kyah Lucas died in February 2022 from complications associated with burns she sustained while receiving care from support workers employed by LiveBetter in her home in Orange, New South Wales.

The NDIS Commission alleged that LiveBetter failed to comply with its obligations under the National Disability Insurance Scheme Act 2013, the NDIS code of conduct and its practice standards. LiveBetter subsequently admitted liability in a statement of agreed facts.

The Federal Court ordered LiveBetter to pay civil penalties to the commonwealth totalling $1,800,000 and NDIS legal costs.

NDIS Minister Bill Shorten said disability providers must do everything they could to keep participants safe.

‘LiveBetter failed to look after Kyah Lucas’, said Mr Shorten. ‘She was a vulnerable woman who needed support, safeguarding and care.

‘We want to send a strong message that those entrusted with the care of NDIS participants will be held to the highest standards.’

Acting NDIS Quality and Safeguards Commissioner Michael Phelan said Ms Lucas’s tragic death should have been avoided, and the court’s decision is a warning to other disability-service providers.

‘The findings from this proceeding put all NDIS providers on notice that they need to pick up their game and ensure their staff are properly trained and highly competent’, he said.

‘All disability providers and support workers must have safety front of mind when it comes to supporting people with disability. We will not hesitate to take action where providers fail to keep people with disability safe.’

The NDIS Commission has strong regulatory and compliance powers under commonwealth law where suspected breaches of a provider’s obligations under the NDIS act, including the NDIS code of conduct and its practice standards, are identified.

Powers include seeking civil penalties when a provider has failed to deliver support and services in a safe and competent manner.

NDIS acts against Oak Tasmania

The NDIS Commission has begun civil penalty proceedings against Oak Tasmania for contraventions of the National Disability Insurance Scheme Act.

The commission has alleged that Oak Tasmania failed to comply with its conditions of registration and the NDIS code of conduct in providing support and services in a safe and competent manner.

Alleged incidents include failing to provide access to adequately trained support staff, failing to manage properly risks to participants, failing to administer properly medical devices and medication, and failing to supervise an adolescent in their care.

The NDIS Commission also alleges that Oak Tasmania failed more than six hundred times to report incidents, including some that involved serious injury and neglect, within the required timeframes by law.

Acting NDIS commissioner Michael Phelan said the scheme took allegations of conduct affecting the safety of NDIS participants, including the failure to report incidents, very seriously.

‘The NDIS code of conduct applies to all providers and workers for very good reason. To keep everyone safe’, he said.

‘Providers must ensure their staff are properly trained and that any injuries or harm suffered by participants are promptly reported to the NDIS Commission as required under the NDIS rules.

‘The [commission] will hold accountable any provider that does not comply with the law.’

Tip-offs helping to catch NDIS fraudsters

There has been a significant increase in the number of fraud tip-offs to the National Disability Insurance Agency since the set up of the Fraud Fusion Taskforce in November 2022.

In the December quarter, the NDIA received 4667 tip-offs about fraud and compliance issues – an increase of more than 75 per cent on similar quarters before the FFT was set up. The trend has continued, more than two thousand tip-offs having been received in the month of February alone.

Two major prosecutions have highlighted the role that all Australians can play in preventing fraud against the NDIS.

In one investigation, tip-offs led to two women being charged, one pleading guilty and another found guilty at trial.

One of the women falsified reports and overcharged for services. She was found guilty of twenty-two fraud-related offences.

Charges included dishonestly obtaining a financial advantage from the commonwealth of an alleged value of more than $1 million.

The second investigation resulted in a woman being jailed for three-and-a-half years for her involvement in an attempt to defraud the NDIS.

The NDIA had investigated the Queensland case after receiving complaints that people had been claiming for services that they never actually provided. Four people were arrested and charged, all four pleading guilty to general dishonesty against the commonwealth.

‘Since commencing in 2022, the Fraud Fusion Taskforce has investigated more than 100 cases [involving] over $1 billion of NDIS funding’, minister Shorten said.

Anyone with information about suspected fraud involving the NDIS should contact the scheme’s fraud helpline on 1800 650 717 or email fraudreporting@ndis.gov.au.

UK charity-fraud insights

More than a third of charities said that they had experienced more instances of fraud in 2023 than in 2022, the giant transnational firm BDO has reported.

The 2023 Charity Fraud Report details the findings from BDO’s annual survey conducted with the independent, non-government UK Fraud Advisory Panel.

The impact of fraud is not just financial. Fraud affects all parts of an organisation, from staff turnover to negative press and reputational damage.

Charity fraud statistics:

- 36 per cent of charities said that they had experienced more instances of fraud than last year

- 43 per cent reported fraud or attempted fraud

- 67 per cent agree that the cost-of-living crisis had increased fraud risk

- 50 per cent of detected frauds were perpetrated by staff, members, volunteers, or trustees

- 92 per cent of charities that suffered a fraud was hurt financially

- 56 per cent experienced non-financial issues

- 45 per cent suffered a loss of morale amongst staff, volunteers and trustees, and

- 64 per cent expected fraud-risk to increase in the next 12 months.

The report describes how UK charities view fraud risk, the losses that can be sustained, what measures charities can put in place to combat fraud risk. The findings and recommendations have relevance here.