We are happy to present the quarterly instalment of our mid-market M&A overview. The analysis focuses on the current quarter intending to provide you with a brief overview of recent mid-market M&A activity.

Overview

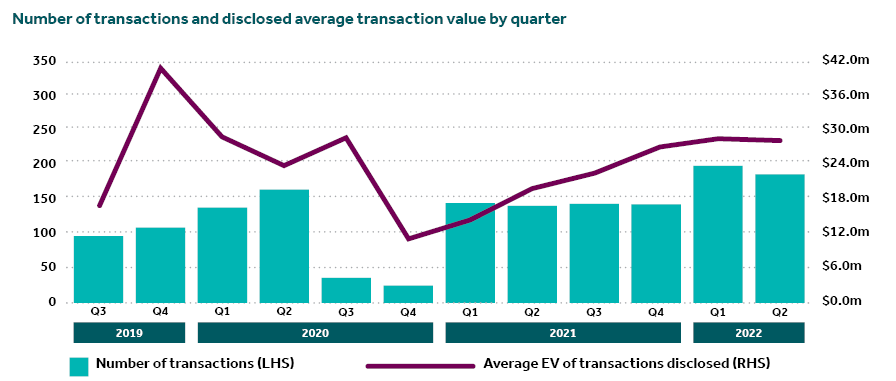

The number of transactions in Q2 FY2022 decreased slightly on the previous quarter and was significantly higher on the same quarter in the prior year.

The average deal size decreased slightly from $28.5 million in Q1 FY2022 to $28.1 million in Q2 FY2022, a decrease of 6%. Over the last 12 months, the average deal size was up from $24.7 million to $26.6 million, an increase of 8% from the average deal size for the prior 12 months. The increase in the average deal size was the result of greater average deal sizes since Q4 FY2021.

Sector

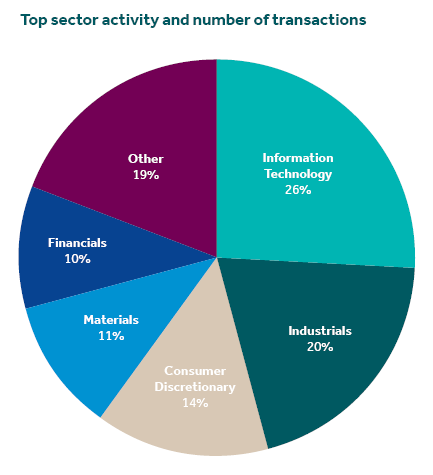

Information technology (26%), industrials (20%) and consumer discretionary (14%) were the most active sectors during the quarter, followed by materials (11%) and financials (10%). Combined, the top 5 sectors represent 80% of all transactions completed in the quarter.

M&A activity in the information technology sector continued to be strong albeit a slight decrease in Q2 FY2022, which had 43 transactions compared to 44 in quarter prior. Other significant sectors were the industrials sector, which had 34 transaction, representing a 6% increase from the previous quarter, and the consumer discretionary sector which had 25 transactions, representing an 11% decrease on last quarter.

Geography

Overseas acquirers represented 30% of all transactions. The United States and the United Kingdom were the largest acquirers of Australian companies representing 12% and 6% respectively of all acquisitions in the quarter. China, followed by New Zealand were also actively acquiring Australian companies on a slightly smaller scale.

Overseas acquirers were active across the information technology, industrials, materials, consumer discretionary and communication services sectors, representing 85% of total overseas transactions.

EBITDA multiples

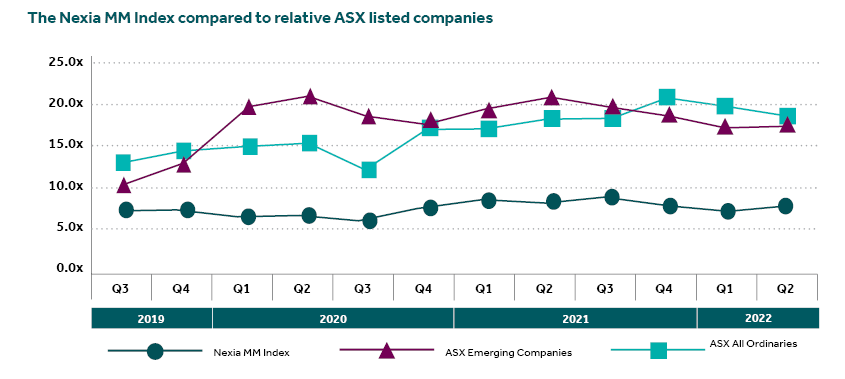

The Nexia MM Index (see below regarding methodology and limitations) is compared to relative ASX indices in the graph.

The ASX Emerging Companies index increased by 3% and ASX All Ordinaries index decreased by 9% from the prior quarter. The Nexia MM Index increased by 7% in the current quarter.

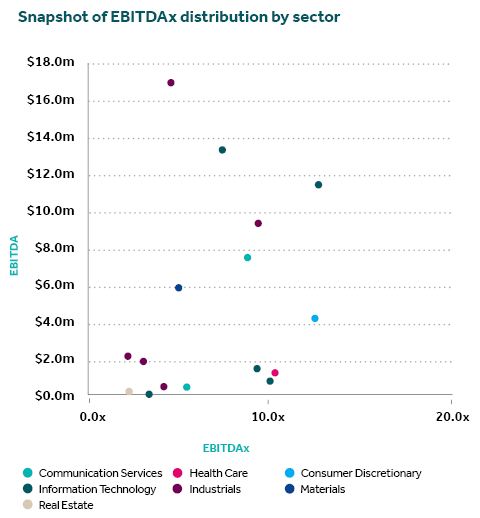

One transaction can have a significant impact on the Nexia MM Index. To provide more insight into the Nexia MM Index, we have highlighted the EBITDA and capitalisation multiple of some of the transactions.

Although the same limitations apply to this analysis as the overall index, the study bears the relationship between multiples and size with lower EBITDA generating companies also receiving a lower multiple. It also provides an insight into the relative sector multiples.

Methodology

The analysis was prepared based on data sourced from S&P Capital IQ at the end of each quarter. Our data set has not been updated for transactions that may be added to S&P Capital IQ retrospectively as data becomes available. Data analysed is for completed transactions, with a primary geographic location in Australia and an implied enterprise value of less than $200 million from 1 October 2019 to 31 December 2021. Transactions where no value was disclosed is included in the volume data with the implicit assumption that these would relate to smaller transactions and therefore meet the criteria.

Overall 1,513 transactions are included within the data analysed. Transaction values were disclosed for 670 (44%) of these transactions with an aggregated transaction value of $25.4 billion. 77 transactions (5%) had sufficient data disclosed to calculate the EBITDA multiples.

In respect of our methodology, we note that this is a simple analysis to give an overview of the market and potential movements. It should in no way be seen as a substitute for a rigorous review of any potential opportunity that you may be considering and you should seek appropriate professional advice for your circumstances.

We note that the source data is limited by the amount of information that is made public and captured in the S&P Capital IQ database. The calculations we have performed, in particular due to the limited number of data points in respect of EBITDA multiples, can be heavily influenced by a single transaction which reflects that transaction’s particular circumstances rather than a reflection of the market as a whole.

Analysis of all transactions, including sector and buyer location is based on S&P Capital IQ classifications.

About the Nexia MM Index

The Nexia mid-market EBITDA multiple (Nexia MM Index) analysis is a simple analysis of EBITDA for acquisitions of unlisted mid-market companies where the data is reported. It is indicative of a trend in the overall market rather than implying the multiple that should be considered for a particular company. The Nexia MM is limited by a number of factors, including that there are a small number of transactions in Australia where the data is available. As a result the average EBITDA multiple can be significantly influenced by individual transactions where the specific characteristics of the transaction may have resulted in a higher or lower multiple than would otherwise be achieved. To minimise the impact we have shown a rolling annual EBITDA multiple for disclosed transactions above.

Considering the data against the listed company comparative, the Nexia MM is based on acquisitions and therefore implicitly reflects a control premium whereas the multiple for the listed companies reflect a portfolio interest.

The range in the identified EBITDA multiples is significant at 2.6x to 12.3x in FY2019, 2.6x to 22.0x in FY2020, and 0.2x to 37.8x for FY2021. The current range for FY2022 is 2.6x to 42.3x.

Contact us

If you would like to discuss further any of the information provided in this update and how it will impact you, please contact your Nexia Adviser.