Current GST Problem

Currently, whenever new residential premises are sold, 10% of GST is included in the sale price (i.e. the purchaser pays over an amount equal to the GST to the developer as part of the sale price) and then the developer is supposed to remit the GST so charged to the Australian Taxation Office (ATO) within a maximum period of 3 months.

Unfortunately, if developers engage in “phoenix activities” (i.e. generally activities where developers claim GST input tax credits on their construction costs, but liquidate their operations before they have to remit the GST they charged on the sale of the new residential premises) - the ATO will lose out on that GST.

Proposed solution from 1 July 2018

In an attempt to curb this kind of GST exploitative behaviour, the Australian Government proposes to make the purchaser responsible for withholding an amount of 1/11th of the GST inclusive purchase price as GST and pay that amount directly to the ATO on settlement for the new residential premises (as opposed to the current treatment where 1/11th is first paid to the developer who then has the obligation to remit that amount to the ATO – but frequently does not).

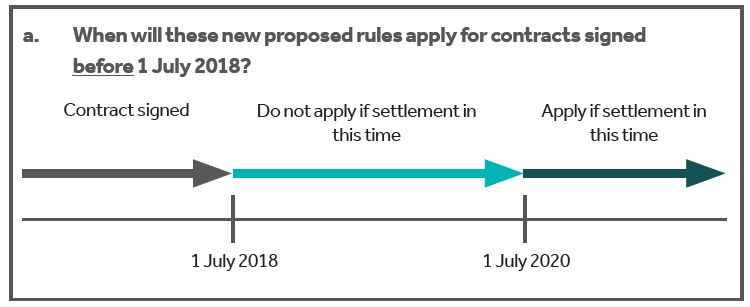

The proposed change – if enacted – is slated to apply to all sale contracts of new residential premises and subdivided residential lots settled on or after 1 July 2018. However, there is an exception for contracts signed before 1 July 2018:

- If settlement occurs before 1 July 2020 – these new proposed measures will not apply (i.e. there will still be an obligation on the developer to remit the GST);

- If settlement occurs on or after 1 July 2020 – these new proposed measures will apply (i.e. there will now be an obligation on the purchaser to pay the amount of GST directly to the ATO on settlement)

What do these proposed changes mean for you?

At the time of writing, the measures mentioned above are only proposals by the Government and not yet law.

However, should these proposals become law in its current format, the direct payment of GST by the purchaser to the ATO on settlement may cause cash flow and compliance issues for developers (because developers will lose out on the extra cash buffer of GST that only has to be remitted to the ATO up to a maximum of 3 months after settlement).

Likewise, should the new residential premises be sold subject to the margin scheme (i.e. broadly a scheme where GST will not be paid on 1/11th of the sale price but only on 1/11th of the difference between the sale price and the purchase price), the purchaser will be required to withhold and pay 1/11th of the purchase price (i.e. sale price charged by the developer) to the ATO.

By allowing the purchaser not to apply the margin scheme when paying over the GST to the ATO, there will effectively be an overpayment of GST to the ATO (i.e. GST should have been charged on the margin and not just on the full sale price) which may also lead to cashflow problems for the developer until the overpayments have been recovered from the ATO.

Nexia Australia will keep you updated on any new developments.