How a six-year itch can influence your tax consequences

Sometimes a situation may arise where you may want to move out of your home that you primarily reside in (i.e. your main residence) and live somewhere else while keeping the original property as an investment.

You may consider such a move out of your home if:

- You have been relocated for work;

- Depending on the stage of your life, you either want to downsize (e.g. the so-called empty nesters whose children have left home) or upsize (e.g. you have a young family with children still living at home) where you live;

- You are experiencing financial difficulties and would rather move somewhere cheaper while you hope that most of your mortgage will be paid by your new tenants.

In such a situation your former main residence may become an investment property. Such a change in the way the property is used may give rise to different tax consequences.

This fact sheet discusses some of the most important tax consequences when you convert your main residence into an investment property (or vice versa).

What are the primary tax considerations when converting a main residence into an investment property (or vice versa)?

Tax deductions for investment properties

The general rule is that you can only deduct rental expenses that were incurred to derive income from an investment property (provided these expenses were not of a private or capital nature).

These types of expenses can either be deducted immediately or over time – depending on what type of expenses they are.

Rental expenses for which you can claim a tax deduction immediately

Examples of expenses that may be immediately deductible include:

- Interest paid as part of the loan repayment;

- Cost of advertising for tenants;

- Lease document expenses (e.g. preparation, registration and stamp duty) and legal expenses (excluding acquisition costs and borrowing costs);

- Repairs and maintenance and travel expenses (to collect rent, to inspect property or to maintain property);

- Body corporate fees and charges (for administration and maintenance but not for capital expenditure);

- Council rates, insurance (buildings, contents, public liability), water charges;

- Borrowing expenses of $100 or less (over time if more than $100);

- Fees paid to a managing agent; and

- Depreciating assets costing $300 or less (over time if costs more than $300).

Rental expenses for which you can claim a tax deduction over time

Examples of expenses that may only be claimed over a number of income years include:

- Borrowing expenses (e.g. loan establishment fees, title search fees, mortgage broker fees, stamp duty charged on mortgages) of more than $100 is spread over the lesser of 5 years or the term of the loan;

- Amounts for the decline in the value of depreciating assets over their effective live (if costs more than $300); and

- Capital works deductions whereby the cost of investment properties can basically be depreciated over 40 years (2.5%) and in some cases 25 years (4%).

Expenses for which you cannot claim a tax deduction

Examples of expenses for which you cannot claim a deduction include:

- Acquisition and disposal costs of the property (because they are capital in nature) with the exception of stamp duty in the ACT;

- Expenses not incurred by you (e.g. water or electricity charges the tenants have paid); and

- Expenses not related to the rental of a property (e.g. private expenses incurred by you when you use your holiday home during the time it is not rented out).

Capital gains tax (CGT) consequences

CGT main residence exemption

When you sell your main residence for more than its cost, any capital gain will be exempt from CGT (either fully or partially).

In broad terms, you will qualify for a full CGT main residence exemption if:

- You have used the property as your home for the whole period of ownership;

- During this period, you never used the property to produce assessable income (e.g. rental income or used the property to derive business income); and

- The land on which the property is situated is 2 hectares or less.

Subject to the 6 year absence rule that will be discussed below, you will qualify for a partial CGT main residence exemption for only the period you actually used the property as your main residence.

This means that you will have to pay CGT on the capital gain relating to the period the property was not used as your main residence.

However, note that the calculation of the eventual CGT liability is different depending on whether you:

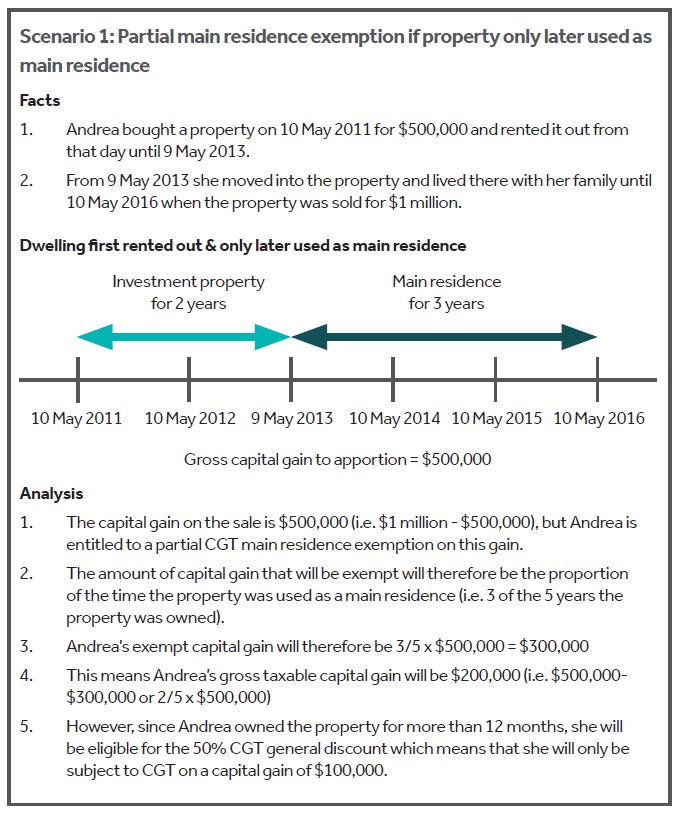

- First used the property as an investment property and only later used it as a main residence (apportion the capital gain based on time1); or

- First used the property as a main residence and only later used it as an investment property (deem new cost base2 and calculate capital gain – do not apportion capital gain based on time).

Set out below are worked examples illustrating the different CGT consequences in these 2 scenarios.

6 year absence rule

Normally, a property can only be your main residence if you live in the property and treat it as your main residence.

However, under the 6 year absence rule, you can still treat the property as your main residence even if you are absent from the property indefinitely if the property is not rented or up to a maximum of 6 years if rented.

This concession is very generous and is particularly relevant for individuals who are considering moving out of their home to live elsewhere. A move such as this should be made for a good reason (e.g. because you are going overseas for your work), otherwise the 6 year absence rule may not apply.

The 6 year period is also reset each time an owner moves back into the property and starts using the house as a main residence again (so you can have multiple six-year itches).

You can only have one property eligible for the main residence exemption at a point in time. If you have two or more properties that would potentially qualify for the main residence exemption, you would need to elect which one is to be the main residence for that period.

Final thoughts

This fact sheet only broadly examined some of the main tax factors involved when turning your main residence into an investment property (or vice versa).

Since tax issues affecting property transactions can be a very complicated area, we would encourage you to seek professional advice on any property transaction you may contemplate.

If you may be affected by anything mentioned in this fact sheet, or would like to know more about how tax can affect your property transactions, please speak to your Nexia Adviser.

1 - Section 118-185 of the Income Tax Assessment Act 1997.

2 - Section 118-192(2) of the Income Tax Assessment Act 1997.

3 - This s118-192(2) market value rule seeks to preserve the CGT free status on the capital gain made from the date of purchase to the time when the property ceased being the main residence.