17 FEBRUARY 2019

Proposed Changes in the Superannuation Guarantee Law

High income earners with earnings over $263,157 are at risk of breaching the annual concessional superannuation contribution cap of $25,000, particularly if compulsory superannuation contributions are made by multiple employers. Under current laws employers are required to pay 9.5% of an employee’s salary/wage into a complying superannuation fund. Failure to do so results in the imposition of the superannuation guarantee charge.

Under the soon to be enacted new law, qualifying employees will be able to apply to partially or wholly opt out of the super guarantee regime in respect of one or more employers.

The new law will apply retrospectively from 1 July 2018. Eligible employees whose superannuation guarantee contributions will exceed the $25,000 concessional contributions cap due to their high salary/wage, will need to apply to the ATO for an employer exemption certificate which will notify the ATO that their salary/wage should not be subject to superannuation guarantee contributions. Provided the gross salary/wage threshold is exceeded, the ATO will issue an employer exemption certificate, which releases the employer from the obligation to pay superannuation guarantee. Exemption certificates can be issued for multiple quarters within a financial year but will not extend beyond the end of the financial year. The employee and employer are free to negotiate additional cash or non-cash remuneration in place of the super guarantee contribution. The exemption certificates cannot be varied or revoked after issue.

The new law will assist high income earners by releasing additional cash flow and reduce paperwork for employers and employees in respect of superannuation guarantee compliance. This amendment will also prevent unintended concessional caps breaches caused by excess contributions over the $25,000 cap.

If an employee exceeds the contribution cap, the excess concessional contributions are included in the individual’s assessable income and taxed at marginal rates, but the employee is entitled to a 15% tax offset to reduce their tax payable.

The proposed new law was passed by the House of Representatives on 20 June 2018 and is awaiting consideration by the Senate.

For assistance with your BAS or superannuation speak to your Nexia Adviser.

24 OCTOBER 2018

Super guarantee health check

Following on from our widely read Top Tax Tip on the proposed superannuation guarantee amnesty, we thought it would be a good idea to remind employers of their obligation to pay superannuation guarantee contributions - currently at a minimum rate of 9.5% of ordinary time earnings on behalf of all eligible workers earning $450 or more before tax in a calendar month. Employees include company directors who receive payments in their capacity as a director (and also contractors in certain circumstances).

Ordinary time earnings are generally what employees earn for their ordinary hours of work (e.g. commissions, shift loadings and allowances, but does not include overtime payments).

Superannuation guarantee contributions are usually made quarterly via SuperStream (i.e. a system whereby contributions are made either through electronic funds transfer or BPAY) and the employer will qualify for a tax deduction for such payments if such payments are made to a complying superannuation fund.

The penalties for failing to pay superannuation guarantee contributions are quite severe (i.e. the superannuation guarantee shortfall amounts, interest on those shortfall amounts and an administration fee of $20 per employee per quarter). Please contact us if you have any queries to ensure that the correct amount of superannuation guarantee contributions are paid by the due date.

17 OCTOBER 2018

You may have to lodge your T-BAR report by 28 October 2018

From 1 July 2018, all SMSFs must report the following events that affect their member’s transfer balances that occur after 1 July 2017:

- Commencing retirement income streams.

- Pension commutations.

- Certain limited recourse borrowing arrangement payments.

- Personal injury contributions.

This transfer balance account events reporting (T-BAR) will enable the ATO to determine whether both the $1.6 million transfer balance and total superannuation caps have been breached.

The frequency of T-BAR reporting (e.g. yearly or quarterly) depends on the total super balance of a member within the SMSF (and not the SMSF member balance). Therefore:

- SMSFs with members who have total balances of less than $1 million will only have to report yearly when they lodge their SMSF annual return; and

- SMSFs with a member who has a total super balance of $1 million or more will have to report within 28 days after the end of the quarter in which the event occurs (i.e. 28 October is 28 days after 30 September).

Once the frequency of T-BAR reporting has been set, SMSF trustees will not be expected to move between annual and quarterly reporting, regardless of fluctuations in the members’ balances.

Please contact your Nexia adviser as soon as possible, because there are penalties involved and your transfer balance account may be adversely affected if you do not lodge your T-BAR report on time (e.g. 28 October 2018).

10 OCTOBER 2018

Proposed superannuation guarantee amnesty

There is currently a Bill before the Senate that, when enacted, will provide a once-off 12-month amnesty (i.e. from 24 May 2018 to 23 May 2019) for businesses that failed to make superannuation guarantee payments for workers from 1 July 1992 up to 31 March 2018.

Catch-up payments of missing superannuation guarantee charges disclosed in this amnesty period will not incur penalties and will be tax deductible. However, if employers don’t make any catch-up payments of missing superannuation guarantee charges before 24 May 2019, higher penalties (e.g. minimum 50% on top of superannuation guarantee charge amounts and penalties up to 200% if no superannuation guarantee statements) will be imposed once such employers are eventually caught.

We will keep you updated on any new developments with this superannuation guarantee amnesty measure.

5 SEPTEMBER 2018

The importance of knowing if your worker is a contractor or an employee

Employers must know whether their workers are employees or contractors because the tax, superannuation and other government obligations are different depending on the worker’s status:

- If a worker is an employee, PAYG withholding will need to be withheld from wages. The employer must report and pay the withheld amounts to the ATO, pay superannuation at least quarterly for eligible employees, and report and pay FBT if fringe benefits are provided to employees.

- In contrast, if a worker is a contractor, usually PAYG is not withheld from payments - unless they have not quoted their Australian Business Number (ABN) in which case PAYG withholding must be deducted at the top marginal tax rate. FBT is not payable if non-cash benefits are provided to a contractor. However, depending on the labour services contract or arrangement, especially if the contract is principally for a contractor’s labour, superannuation guarantee contributions must be made to a complying superannuation fund.

Establishing whether a worker is an employee or contractor may be difficult. The whole working arrangement should be examined to determine whether the worker merely works in the business (i.e. an employee) or whether the worker operates their business and performs work for the business (i.e. a contractor).

Incorrectly treating employees as contractors can subject businesses to PAYG withholding penalties and superannuation guarantee charges.

Please contact us if you are unsure of the correct status of your workers.

5 SEPTEMBER 2018

SMSF actuarial certificates

Before the new super rules commenced from 1 July 2017, more Self-Managed Superannuation Funds (SMSFs) were either entirely in retirement or accumulation phase. However, with the introduction of the $1.6 million Transfer Balance Cap (i.e. pension limit) and the Disregarded Small Fund Asset Measures (i.e. the ability for an SMSF to segregate) this meant some members may not be entirely in retirement phase.

From 1 July 2017 onwards, an SMSF will be required to obtain an actuarial certificate where:

- The SMSF is paying a pension that is not an account based pension or retirement phase transition to retirement pension (e.g. a lifetime pension);

- The SMSF is ineligible to use the segregated method as the SMSF has Disregarded Small Fund Assets; or

This is where a member within an SMSF is:

- receiving a retirement phase income stream (which includes income streams from inside the SMSF and also external sources such as defined benefit income streams); and

- has a Total Super Balance of more than $1.6 million the preceding 30 June of the applicable financial year.

This means even where the SMSF is in 100% pension phase, an actuarial certificate will be required to state the SMSF is 100% exempt. - The SMSF has accumulation and retirement phase interests and chooses not to use the segregated method (i.e. segregates specific assets to support pension and accumulation accounts).

Please contact your local Nexia adviser if you have questions about your SMSF.

8 AUGUST 2018

Streamlined superannuation release process to pay additional assessments

Ordinarily, taxpayers can only be paid from their superannuation fund if they reach certain conditions of release (e.g. turned 65, turned 60 and retired, reached preservation age and retired with no intention to be gainfully employed, has permanent incapacity or has a terminal medical condition).

However, as mentioned in a previous top tax tips , an individual has the option to obtain reimbursement from their superannuation fund to pay for additional assessments arising from:

- excess concessional and non-concessional contributions (i.e. contributions exceeding the concessional cap of $25,000 or non-concessional cap of $100,000 a year); and

- Division 293 assessments (i.e. 30% tax on contributions of individuals earning more than $250,000 a year).

A release authority must be prepared to receive such a reimbursement. The process of applying for a release authority has been simplified from 1 July 2018.

Please speak to your Nexia adviser so that we can assist you in applying for a release authority from the ATO to enable you to withdraw money from your superannuation fund to receive reimbursement.

25 JULY 2018

Red flags for SMSF auditor

In the past, we have warned about using cheap so-called “SMSF audit specialists” to audit a taxpayer’s self-managed superannuation fund.

In particular, there may be some risk involved if a taxpayer uses:

- Auditors who both audit and prepare the financial accounts of the SMSF;

- Low cost auditors; or

- Auditors who are related to any member of the SMSF (e.g. recently an SMSF auditor was disqualified for auditing the SMSF of a family member).

We remind our clients to be vigilant of deals that seem too good to be true. The ATO is alert to these low cost auditors and is making appropriate enquiries.

Preparing incorrect accounts and tax returns may cause the SMSF to become non-compliant – giving rise to the SMSF paying tax at 45% of its income and on the value of its assets in the year of non-compliance. Such a high rate of tax will result in a very significant depletion of the SMSF’s assets – therefore SMSFs must be accurate in their reporting and operations.

Your Nexia advisor is always pleased to assist you with any enquiries regarding your SMSF, the pros and cons of having an SMSF and maximising benefits under our tax and superannuation laws.

18 JULY 2018

Illegal early release of superannuation

Individual taxpayers are only allowed to access their superannuation once they have met a condition of release (e.g. turned 65, turned 60 and retired, reached preservation age and retired with no intention to be gainfully employed, has permanent incapacity or has a terminal medical condition).

A SMSF trustee that releases superannuation funds early (i.e. before a condition of release has been met) may be disqualified as trustee, have administrative penalties imposed or may be subject to prosecution. Furthermore, the SMSF may be made non-compliant (i.e. SMSF will then pay tax at 45% of its income and on the value of its assets in the year of non-compliance) – quite severe consequences.

If you have been approached by promoters promising that they can help you access your superannuation early (for a fee), we would strongly suggest that you do not sign any documents or provide them with any of your personal details. Contact your Nexia representative so that we can alert the ATO about this unlawful behaviour.

27 JUNE 2018

Get ready for Transfer balance account reporting (T-BAR)

At 1 July 2017, individuals were only allowed to have $1.6 million of assets in the retirement phase of their superannuation fund (i.e. a limit on the amount of savings/assets that can be in tax free pension phase in superannuation).

Individuals with retirement phase pensions at 30 June 2017 who have an aggregated value (in all superannuation funds) in their member’s accounts between $1.6 and $1.7 million had until 31 December 2017 to reduce their member balance in pension phase to $1.6 million.

To determine whether the $1.6 million transfer balance cap has been breached, pre-existing retirement phase superannuation income streams that a member was receiving on 30 June 2017 and that continued to be paid to them on or after 1 July 2017 must be reported to the ATO on or before 1 July 2018.

From 1 July 2018, all SMSFs must also report the following events that affect their member’s transfer balances that occur after 1 July 2017:

- Commencing retirement income streams

- Pension commutations.

- Certain limited recourse borrowing arrangement payments.

- Personal injury contributions.

The frequency of reporting of above mentioned transfer balance account events (T-BAR reporting) depends on the size of the total amount of superannuation in the SMSF:

- SMSFs with member balances of $1 million or more will have to report within 28 days after the end of the quarter in which the event occurs; and

- SMSFs with member balances of less than $1 million will only have to report yearly when they lodge their SMSF annual return.

This T-BAR reporting will enable the ATO to determine whether both the $1.6 million transfer balance and total superannuation caps have been breached. Your Nexia adviser can assist you with your T-BAR reporting.

20 JUNE 2018

Other Important superannuation issues to consider

Because of the fundamental changes to the superannuation system from 1 July 2017, the following issues need to be considered for the 2018 income tax year:

- The tax-exempt status is removed on income from assets that support a Transition to retirement income stream (TRIS) that is not in the retirement phase. Income from assets supporting a non-retirement phase TRIS will be taxed at 15% regardless of the date the TRIS commenced. However, the TRIS account can enter into retirement phase if the SMSF member has met a nil cashing restriction condition of release (e.g. aged 65 or above, turns 60 and retires, or over the preservation age and retires with no intention to be gainfully employed, has permanent incapacity or has a terminal medical condition). Entering the retirement phase brings the pension exemption but also brings the pension within the $1.6 million transfer balance cap regime.

- Members will only be allowed to make non-concessional contributions if their total superannuation balance in all superannuation funds does not exceed $1.6 million (note; contributions from the small business CGT cap, the $300,000 downsizing contributions and any Court order superannuation splits will not be subject to this $1.6 million total superannuation balance cap,).

- Ensure non-commercial limited recourse borrowing arrangements (LRBAs) to fund the acquisition of properties are put on arm’s length terms (e.g. there must be market interest rates, commercial lending periods and principal and interest repayment arrangements).

Superannuation law is complex. Therefore, please speak to an authorised Nexia representative for advice on these issues.

13 JUNE 2018

Proposal to only audit SMSFs every 3 years instead of yearly

As mentioned in our recent 'Guide to the Federal Budget 2018', from 1 July 2019, SMSFs with a good history of record-keeping and compliance (e.g. SMSFs that have three consecutive years of clear audit reports and have lodged their annual returns on time) will only have to be audited once every three years (i.e. audit 36 months of financial records and compliance with superannuation laws once every 3 years) instead of once every year.

According to the budget proposal, such a switch from a yearly to a three yearly audit requirement will reduce red tape for such SMSF trustees.

However, from a practical perspective, it is uncertain whether this proposed change may lead to cost savings. There may be small cost savings because only one audit report will be required on a three yearly basis, but on the other hand there may be no reduction in audit work involved over the three years (i.e. an auditor will need to review the same number of transactions over the three years).

At the time of writing, the only publicly available official information on this measure is the Federal Budget. Draft legislation is expected in the second half of 2018 and we trust once such legislation is released there will be more details available on how these proposed measures may work.

Nexia Australia will keep you updated on relevant official developments pertaining to this proposal affecting taxpayers that have SMSFs (i.e. currently any information you may have seen regarding this new proposal is purely speculation and not based on official publicly available information released by the Government).

30 MAY 2018

To qualify for deduction for super contribution, money must hit bank account by 29 June

From 2018, both employees and self-employed individuals can claim a tax deduction for personal superannuation contributions, provided the superannuation fund have physically received the contribution by 29 June 2018 (see tip above) and the individual has provided their superannuation fund with a notice of intention to claim (a deduction) document.

If leaving superannuation contributions to the last minute, you need to be aware of exactly how long the superannuation contribution takes to reach a superannuation fund’s bank account – for example if you are paying the superannuation contributions one day before the due date (i.e. 29 June 2018 for the 2018 income tax year, but the payment is not deposited into the superannuation fund’s bank account until 2 days later, no tax deduction will be allowed in the 2018 income tax year.

Please note that if the employer is utilising the ATO small business clearing house, the super guarantee contributions are counted as being paid on the date the clearing house accepts them (provided the fund does not reject the payments).

Also, be careful if the retail superannuation fund closes off their acceptance of contributions before 30 June.

An easy way to prevent any of these late payment issues is to simply pay superannuation contributions at the beginning of June each year, cashflow permitting.

8 MAY 2018

Have you breached the $1.6 million superannuation transfer balance cap?

On 1 July 2017, individuals were only allowed to have $1.6 million of assets in their member’s account in pension phase; any amount in excess of $1.6 million should have been transferred into accumulation phase or withdrawn from the super fund. Pension phase is when a superannuation fund member is in receipt of a pension except for a transition to retirement pension.

Amounts in pension phase exceeding the $1.6 million had to be transferred back to accumulation phase (where the income on such assets is taxed at 15%) by 30 June 2017 (if the excess at 1 July 2017 was more than $100,000) or after 6 months (i.e. by 31 December 2017 if the excess at 1 July 2017 was $100,000 or less).

To neutralise the benefits of having an excess in the tax-free retirement phase, notional earnings (worked out by the ATO by applying a daily accrual of general interest charge (GIC) on the excess) are subject to an excess transfer balance (ETB) tax of either 15% (for first breach of the cap) or 30% (for breaches of the cap from 1 July 2018 onwards).

The ATO has now started issuing ETB tax assessments to SMSF members – if payment is not made within 21 days after this assessment is issued, GIC will accrue on any outstanding payments.

Please speak to your Nexia representative to discuss ways of ensuring this liability is paid on time; this can be done by using assets outside of superannuation or by using superannuation assets to make a large one-off pension payment, make additional commutation of income steams or to take a lump sum of any accumulation interest.

11 APRIL 2018

Send us your information for your SMSF returns

The new superannuation tax law changes mean that preparing your superannuation funds financial statements and tax returns is taking longer this year. Therefore, please send to us your SMSF information for your SMSF’s 2017 accounts and tax return as soon as possible. The ATO have extended the lodgement deadline for SMSFs this year because of this additional work. Trustees of SMSFs must lodge their annual returns by 2 July 2018.

28 MARCH 2018

SMSFs and non-arm’s length income

SMSFs must transact on an arm’s length basis (e.g. the purchase and sale price of SMSF assets should always reflect the true market value of both the SMSF asset and returns). Any non-arm’s length income will be taxed at the highest marginal tax rate.

Furthermore, individuals who have used their self-managed superannuation funds (SMSFs) to borrow from related parties to fund the acquisition of properties – usually through using non-commercial limited recourse borrowing arrangements (LRBAs) must ensure that those borrowing arrangements are on arm’s length terms (e.g. there must be market interest rates, commercial lending periods and principal and interest repayment arrangements).

We can assist you in restructuring your borrowing arrangements to minimise the risk that income generated from the LRBA will be taxed at 47% as non-arm’s length income (NALI).

7 MARCH 2018

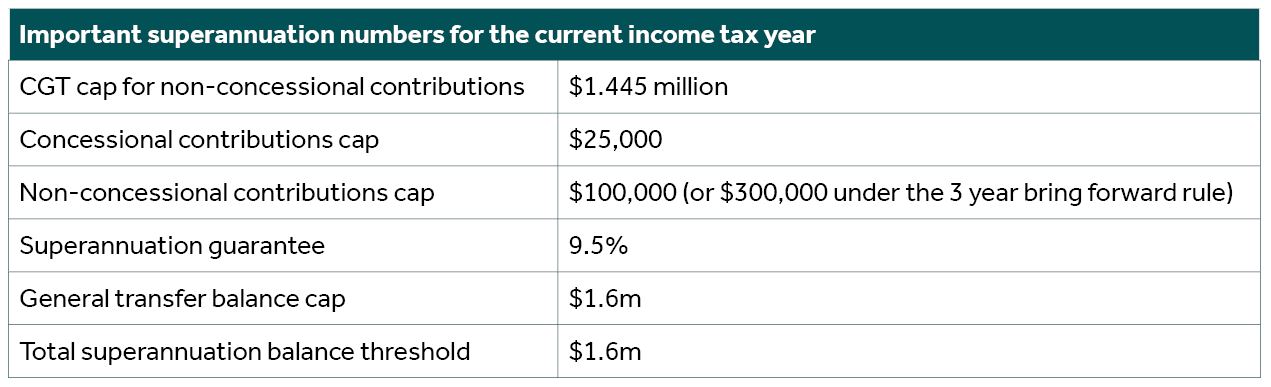

Superannuation rates & thresholds for current year

Fundamental changes have been made to the superannuation landscape from 1 July 2017 (i.e. the current income tax year).

Below is a short summary of the most important superannuation rates and caps that apply for the current income tax year:

Please speak to your authorised Nexia representative if you are not sure what all these numbers mean or what superannuation strategies may be best suited to your circumstances. For more information on these changes also please see our Superannuation Update here.

7 FEBRUARY 2018

Digital changes coming to the small business superannuation clearing house

From 26 February 2018, the Small Business Superannuation Clearing House (SBSCH) will operate on a new ATO digital platform that will enable users of the SBSCH to access the portal with a single new logon.

Because of the transition to a new digital platform - there will be no access to the SBSCH from Tuesday 20 February to Sunday 25 February to allow data to be transferred between the old and the new system - we would advise employers to make their super guarantee payments before the close of business Monday 19 February 2018 to prevent any confusion.

Please contact your Nexia adviser for more information on how to access the new look SBSCH from Monday 26 February 2018.

31 JANUARY 2018

Don’t cut corners when making binding death benefit nominations

On the death of a person, the balance of that person’s superannuation will not automatically form part of the deceased estate - that is, superannuation balances are not automatically distributed according to a deceased’s will.

A valid binding death benefit nomination (BDBN) determines how superannuation death benefits will be distributed (e.g. as a reversionary pension to a dependant, as a superannuation death benefit to a dependant, a non-dependent child or as a payment of an amount to a person’s legal personal representative so that the superannuation balance can be dealt with according to the will of the deceased).

A BDBN not made according to BDBN requirements (e.g. not made writing, not signed in the presence of two witnesses over 18 years of age who are not potential beneficiaries, not containing a signed witness declaration and not sent to the trustee) may lead to BDBNs being invalid resulting in the death benefit nomination being rejected – causing delays and uncertainty about the payment of the death benefit – not an ideal situation!

Please speak to your authorised Nexia representative about the most effective way to manage your superannuation and how we can assist you to ensure you comply with all the requirements for a BDBN to be effective.

31 JANUARY 2018

SMSF audits: If it’s too cheap, it’s probably more trouble than it’s worth

A number of our Nexia clients have received cold calls from various so-called “SMSF audit specialists” offering entire SMSF compliance and audit services for as little as $990. Another supposedly fantastic offer includes being able to do a paperless SMSF audit for as little as $300 within 4 business days. The ATO has warned that if an offer is too good to be true then that is probably the case.

Preparing the financial accounts, having them audited and preparing an SMSF’s income tax return requires a thorough knowledge of our complex income tax and superannuation laws. All entries on the accounts and tax returns must be accurate otherwise the SMSF may be at risk of an ATO audit that may discover incorrect treatment of tax free and taxable amounts payable by the SMSF on the retirement or death of a member.

Preparing incorrect accounts and tax returns may cause the SMSF to become non-compliant – giving rise to the SMSF paying tax at 45% of its income and on the value of its assets in the year of non-compliance. Such a high rate of tax will result in a very significant depletion of the SMSF’s assets – therefore SMSFs must be accurate in their reporting and operations.

We remind our clients to be vigilant of deals that seem too good to be true. Fortunately, the ATO is investigating the low-fee offers because the ATO is well aware of the work involved in preparing accurate accounts and tax returns for SMSFs. Your Nexia advisor is always pleased to assist you with any enquiries regarding your SMSF, the pros and cons of having an SMSF and maximising benefits under our tax and superannuation laws.

24 JANUARY 2018

Due date for lodgement of 2017 SMSF returns only 30 June 2018

Following the fundamental changes to the superannuation landscape that applies from 1 July 2017 (as reported in previous top tax tips and a detailed Nexia tax update on the Superannuation changes), the ATO has extended the due date for lodgement of 2017 SMSF annual returns from 15 May 2018 to 30 June 2018.

This extension of time is good news for SMSFs because now they will have more time to consider and make relevant elections to ensure they fully utilise the transitional CGT relief available for SMSFs.

This CGT relief is necessary because if the balance of a member’s superannuation account was in retirement phase and was valued at more than $1.6 million on 30 June 2017, the superannuation law required that the excess be commuted before 1 July 2017 to either accumulation phase (where earnings are taxed at 15%) or taken outside of superannuation (where earnings are taxed at the individual’s marginal tax rate). The CGT relief is accessed via CGT elections that are evidenced when the SMSF annual return is lodged – now by 30 June 2018.

The CGT election enables SMSF trustees who had part of the super fund in retirement phase at 9 November 2016 to elect for certain assets to be treated as if they were sold and reacquired for CGT purposes on 30 June 2017. The rules differ for SMSFs whose assets were segregated at 9 November 2016, compared with those funds that were using the proportionate method. The CGT election can be made on an asset by asset basis. The election crystallises the capital gain on the SMSF assets, thus resetting the cost base at 30 June 2017. However, the election will not be beneficial in all situations and therefore care should be taken when making the election.

The CGT rules are complex and require detailed consideration. Please speak to your Nexia adviser for assistance.

20 DECEMBER 2017

New reporting obligations for SMSFs

Currently, SMSFs only have to lodge an SMSF annual return that reports on a member’s income tax, regulatory and member contributions.

However, from 1 July 2018, SMSFs will also be required to lodge a Super transfer balance account report (TBAR) that will report transactions to ensure the $1.6 million transfer balance pension cap and the $1.6 million total superannuation balance cap is not breached.

Although SMSF TBAR reporting only applies from the next financial year, all income stream valuations and decisions for the current 2018 year must be documented. We can assist you to help you keep track of the balances in your SMSF.

13 DECEMBER 2017

Superannuation: Ensure you only have $1.6m in pension phase by 31 December

Under transitional rules, SMSF members who have exceeded their $1.6 million transfer balance pension cap by $100,000 or less by 1 July 2017, have until 31 December 2017 to rectify the situation.If not rectified by the due date, members will receive an excess transfer balance determination and incur excess transfer balance tax from the ATO in January 2018.

If you are in excess of the $1.6 million transfer balance cap, please speak to us about possible ways to debit your transfer balance account or whether any alternative strategies are available to legally avoid the excess transfer balance tax.

6 DECEMBER 2017

Beware of SMSF schemes

The ATO is currently scrutinising the self-managed superannuation fund (SMSF) industry and have identified a variety of schemes directed towards minimising or avoiding tax through channelling money inappropriately through SMSFs.

For example, in a previous Top Tax Tips, we have referred to an SMSF scheme that attempts to divert personal services income to an SMSF so that the income will either be exempt from tax (if in pension phase) or at least concessionally taxed (i.e. taxed at 15% as opposed to the individual’s marginal tax rate).

Taxpayers involved in such illegal schemes can face severe penalties under both taxation and superannuation laws and potentially lose 45% of their retirement savings or their rights as trustee to manage their SMSF.

Although you may not have been involved in such a scheme, we are obliged to alert you in case you are ever contacted to enter into such schemes. After all, forewarned is forearmed!

25 OCTOBER 2017

Do not be confused between the $1.6 million transfer balance and total super balance cap

On 1 July 2017, a superannuation fund’s member’s balance in pension phase cannot exceed $1.6 million. Any income on that member balance used to fund a pension is tax free.

This $1.6million transfer balance cap is not influenced by pension drawdowns or accrued growth or losses on assets (i.e. the assets can grow in value without affecting the $1.6million cap.) Let’s say that the $1.6 million grows to $2 million, the income derived by the super fund on the $2 million balance in pension phase is exempt from tax.

In the case of a super fund member who has exceeded the $1.6 million cap, possibly due to having a balance in another super fund for the year ending 30 June 2017, excess transfer balance tax is payable on the income derived from the investment of the excess over $1.6 million. The tax payable on that income is 15% on the first breach and higher rates of tax for subsequent breaches.

However, super fund members who only exceed the $1.6 million transfer balance cap by $100,000 or less have until 31 December 2017 to ensure that their transfer balance cap is only $1.6 million (i.e. they have an extra 6 months from 1 July 2017 to transfer the excess balance either to accumulation phase or draw the excess from the super fund).

Conversely, the $1.6 million total superannuation balance cap comprises the sum of the values of retirement and accumulation phase balances (therefore, unlike the transfer balance cap, fluctuations in asset values and pension drawdowns are taken into account).

The balance of the total superannuation cap is determined at 30 June each year to be applied to the next income year. If a super fund member exceeds the $1.6 million cap, the member cannot make any more non-concessional contributions in the next income year.

With the changed superannuation landscape that now exists from 1 July 2017, obtaining accurate and appropriate advice to your circumstances from our Nexia authorised representatives.

18 OCTOBER 2017

Outstanding tax debt? We can help you set up a payment plan

We would strongly encourage any business with current outstanding tax debts to engage with your Nexia representative to ensure outstanding tax debts are paid in a timely and affordable manner. We can assist a business in establishing a payment plan with the ATO to avoid or minimise penalties and late interest charges on outstanding tax debts, or alternatively your Nexia representative can arrange solutions to refinance and restructure your debts, in order to manage your cashflow.

While having an ATO payment plan, you still need to lodge all of your ongoing activity statements and tax returns on time and the ATO will expect tax liabilities arising from those lodgements to be paid.

11 OCTOBER 2017

SMSF audits: If it’s too cheap, it’s probably more trouble than it’s worth

A number of our Nexia clients have received cold calls from various so-called “SMSF audit specialists” offering entire SMSF compliance and audit services for as little as $990. Another supposedly fantastic offer includes being able to do a paperless SMSF audit for as little as $300 within 4 business days.

Preparing the financial accounts, having them audited and preparing an SMSF’s income tax return requires a thorough knowledge of our complex income tax and superannuation laws. All entries on the accounts and tax returns must be accurate otherwise the SMSF may be at risk of an ATO audit that may discover incorrect treatment of tax free and taxable amounts payable by the SMSF on the retirement or death of a member.

Preparing incorrect accounts and tax returns may cause the SMSF to become non-compliant – giving rise to the SMSF paying tax at 45% of its income and on its assets in the year of non-compliance. Such a high rate of tax will result in a very significant depletion of the SMSF’s assets – therefore SMSFs must be accurate in their reporting and operations.

We remind our clients to be vigilant of deals that seem too good to be true. Fortunately, the ATO is investigating the low-fee offers because the ATO is well aware of the work involved in preparing accurate accounts and tax returns for SMSFs. Your Nexia advisor is always pleased to assist you with any enquiries regarding your SMSF, the pros and cons of having an SMSF and maximising benefits under our tax and superannuation laws.

4 OCTOBER 2017

Pension transfer balance account reports (T-BARs) due soon unless exception

From 1 October 2017, a new T-BAR reporting regime applies to ensure individuals do not exceed their $1.6 million transfer balance cap in respect of their superannuation balances. Pursuant to this regime, certain movements in the pension account (e.g. retirement income streams, commutations, certain limited recourse borrowing arrangement payments) need to be reported within 10 days of the end of the month when the movement occurred.

There is however an exception for SMSFs – the T-BAR reporting regime will only be compulsory for SMSFs from 1 July 2018.

27 SEPTEMBER 2017

Take care when setting up a reserve in your SMSF

From 1 July 2017, the main limits and restrictions on the amount an individual can have in superannuation are:

- the $1.6 million transfer balance cap whereby the balance of a taxpayer’s benefit transferred to the tax free pension account must be limited to $1.6 million; and

- the $1.6 million total superannuation balance cap whereby non-concessional contributions will no longer be possible where the total superannuation balance is $1.6 million.

Some are contending that these limits can be circumvented with the use of reserves.

However, please note that establishing and maintaining such reserves may not be appropriate. The ATO has announced that they will be closely monitoring SMSFs that establish reserves following the introduction of the new limits.

Please contact us so that we can assist you in implementing a superannuation strategy that does not breach the rules.

28 JUNE 2017

Dire consequences if minimum pension payments are not made by 30 June 2017

SMSF trustees with members in pension phase are reminded to make their minimum pension payments by 30 June 2017.

If a trustee fails to make these minimum pension payments by 30 June 2017, the pension account will no longer deemed to be in retirement phase for the whole of the 2017 income tax year – which means the income earned in the pension account will no longer be tax exempt for 2017 – a catastrophic result.

Flow-on effects from such a compliance oversight may also affect s fund’s ability to claim transitional CGT relief as well as impact the changes to the transition to retirement income streams (TRIS) rules commencing 1 July 2017.

14 JUNE 2017

What to do with automatic reversionary and death benefit pensions pre 1 July 2017

Reversionary pensions are usually paid to the spouse of a deceased member of a superannuation fund.With the advent of the new superannuation laws applying after 1 July 2017, concern has been expressed that the balance in the deceased member’s account that has been transferred to the surviving spouse’s superannuation account may cause that person’s account to exceed the new $1.6 million limit.

Where the surviving spouse is receiving a reversionary pension at or before 30 June 2017 and their total superannuation balance exceeds $1.6 million, they may transfer the excess to their accumulation account.The decision to do so must occur before 1 July 2017 and be recorded in relevant documentation.

In contrast, a reversionary pension that breaches the $1.6 million transfer balance cap after 1 July 2017 cannot be retained in accumulation and must be paid out of superannuation (i.e. cashed out).

The above rules apply equally to death benefit pensions paid by a superannuation fund.

7 JUNE 2017

More deductions for contributions to superannuation from 1 July 2017

From 1 July 2017, more people (e.g. contractors or employees) will be able to claim deductions for personal superannuation contributions because they will no longer need to satisfy the requirement to derive less than 10% of total income from salary or wages.

Practically this means that from 1 July 2017 all employees aged 75 or younger may claim a deduction for personal superannuation contributions provided total employer and employee contributions do not exceed the $25,000 concessional contributions cap.

7 JUNE 2017

Compliance reviews and $1.6 million transfer balance cap

The ATO generally will not conduct compliance reviews if members of self- managed superannuation funds (SMSFs) take action before 1 July 2017 to remove any excess money from their retirement balance in excess of the $1.6 million transfer balance cap that applies from 1 July 2017.

This commutation can be done either by rolling over the excess into accumulation phase (where earnings will now be taxed at 15%) or withdrawing the excess from the SMSF as a lump sum payment (where earnings will now be taxed at the member’s marginal tax rate).

Because SMSF accounts are only usually finalised after 30 June, a member may not precisely know the value of their retirement balance at 30 June 2017 and may therefore not know the precise amount of excess that will have to be commuted.

Therefore, as a concession, the ATO will not review a commutation that specifies a written methodology to calculate the precise amount (even if the precise amount can only be ascertained after 30 June 2017 based on historical data). An example of an ATO acceptable commutation would be where the trustee makes a written request before 1 July 2017 to commute “amounts on 30 June 2017 in excess of the $1.6 million”. Please note that the decision to commute must be made in writing and cannot be revoked.

Regrettably, the new superannuation rules coming into effect on 1 July 2017 are complex. We would be pleased to assist you with complying with the new rules that apply to members of all superannuation funds, not just self-managed superannuation funds.

31 MAY 2017

Change in contribution caps – Check your pre-tax super contribution

As mentioned in previous top tax tips, from 1 July 2017 the concessional cap (i.e. the before tax contributions cap) will be $25,000 for all individuals regardless of age (for this current financial year, the cap is either $35,000 if 49 years or over or $30,000 for under 49 year olds).

This change means that to avoid a breach of the (lowered) concessional cap (and thereby incurring further taxes), an individual’s total concessional contributions (e.g. employer contributions such as the 9.5% superannuation guarantee charges, salary sacrifice and deductible contributions) should not exceed the new $25,000 cap.In particular, this may mean salary sacrifice arrangements may need to be reviewed before 1 July 2017.

Please contact us to discuss various strategies to avoid breaching the $25,000 concessional cap from 1 July 2017.

31 MAY 2017

Super guarantee health check

Employers are obliged to pay superannuation guarantee contributions - currently at a minimum rate of 9.5% of ordinary time earnings - to all eligible workers earning $450 or more before tax in a calendar month. Employees include company directors who receive payments in their capacity as a director, and also contractors in certain circumstances).

Ordinary time earnings are generally what employees earn for their ordinary hours of work (e.g. commissions, shift loadings and allowances, but do not include overtime payments).

Superannuation guarantee contributions are usually made quarterly via SuperStream (i.e. a system whereby contributions are made either through electronic funds transfer or BPAY) and the employer would qualify for a tax deduction for such payments if such payments were made to a complying superannuation fund. Note, to qualify for a tax deduction in the 2017 income tax year, the contributions due by 28 July 2017 must be received by the recipient superannuation fund before 30 June 2017).

The penalties for failing to pay superannuation guarantee contributions are quite severe (i.e. the superannuation guarantee shortfall amounts, interest on those shortfall amounts and an administration fee of $20 per employee per quarter) Please contact us to ensure that the correct amount of superannuation guarantee contributions are paid by the due date.

24 MAY 2017

Some superannuation issues to consider

As mentioned in previous Top Tax Tips, major superannuation changes commence on 1 July 2017. We recommend that you speak to your superannuation adviser as soon as possible about the effect these changes may have on your financial position.

Some issues to discuss may include:

- Possibility to take advantage of the higher contributions caps pre 1 July 2017;

- Consider whether salary sacrifice arrangements are still beneficial;

- Reducing pensions to comply with the $1.6 million pension transfer balance cap;

- Review of transition to retirement income streams (TRIS); and

- Review of CGT cost bases of assets and whether CGT elections should be made.

17 MAY 2017

Due date for lodgement of SMSF annual returns now 30 June 2017

The ATO has extended the due date for lodgement of SMSF annual returns for the 2016 income tax year to 30 June 2017 (the due date is usually 15 May).Nexia Australia requested this extension because of the extensive amount of work involved in preparing for the major superannuation changes that apply from 1 July 2017.

3 MAY 2017

Who should be assessed on interest income of joint bank accounts?

As a general rule, interest income on a bank account will be assessed to the person who beneficially owns the money in the account. Broadly, a beneficial owner will enjoy the benefits of ownership even if the beneficial owner is not the legal owner (i.e. the person who has legal ownership or title to the asset).

If bank accounts are held jointly, the interest income will be assessed to the account holders in proportion to their beneficial ownership of the money in the account – assumed to be in equal shares unless evidence indicates otherwise.

If a parent operates an account on behalf of a child under 18 who beneficially owns the money in the account (e.g. the parent operates as a trustee), the interest income will be assessed to the child potentially at higher tax rates under the unearned income rules. A trust tax return is usually unnecessary in these circumstances.

However, if the child does not have beneficial ownership of the money (e.g. the parent deposits their money into the account and can make withdrawals from the account to pay for the child’s school and other expenses), the parent, and not the child, will be assessed on the interest income earned from that account.

26 APR 2017

SMSF annual returns due 15 May

Trustees of SMSFs must lodge their annual returns by 15 May 2017 if they are not eligible for the 5 June 2017 lodgement concession date (note this later date is only available for SMSFs that are non-taxable). Payment of tax debts are also due on the 15 May 2017.

15 MAR 2017

Superannuation guarantee payable only on ordinary time earnings

As mentioned in a previous top tax tips, employers are obliged to make contributions to a complying superannuation fund at a minimum of 9.5% of ordinary time earnings (OTE).

Because OTE does not include overtime payments, penalty rates paid for overtime work – as well as the recent proposed changes to penalty rates for overtime work slated to apply from 1 July 2017 – will not be included in the OTE calculation.

1 MAR 2017

Extension of the spouse tax offset to more couples from 1 July 2017

Currently, individuals who make superannuation contributions on behalf of their spouses (i.e. married or de facto) may only claim the spouse tax offset (up to a maximum of $540 a year) provided the spouse is earning a low income (i.e. less than $13,800 a year) or not working.

So that individuals can make greater superannuation contributions for their spouses, the spouse income threshold will be increased to $40,000 from 1 July 2017. However, no offset will be available for the contributing individual if the receiving spouse has either exceeded their non-concessional contributions cap for the relevant year (i.e. for the year ending 30 June 2018 the cap will be $100,000) or has more than $1.6 million in superannuation (i.e. for 2018 the cap will be $1.6 million).

Note also that no offset will be available if an individual first makes a contribution to his/her own superfund and then splits this balance with his/her spouse).

8 FEB 2017

No administrative penalties if admit to fraudulent SMSF scheme before 30 April 2017

In a previous Top Tax Tips, we referred to a self-managed superannuation fund (SMSF) scheme that attempts to divert personal services income to a SMSF so that the income will either be exempt from tax (if in pension phase) or at least concessionally taxed (i.e. taxed at 15% as opposed to the individual’s marginal tax rate).

Please note that anyone who may have entered into such a fraudulent scheme will not be subject to administrative penalties if they make a voluntary disclosure to the ATO before 30 April 2017.

Although you may not have been involved in such a scheme, we are obliged to alert you in case you are ever contacted to enter into such schemes. After all, forewarned is forearmed!

21 DEC 2016

Reminder to restructure your limited recourse borrowing arrangements by 31 January 2017

Individuals who have used their self-managed superannuation funds (SMSFs) to borrow from related parties to fund the acquisition of properties – usually through using non-commercial limited recourse borrowing arrangements (LRBAs) – have until 31 January 2017 to ensure those borrowing arrangements are on arm’s length terms (e.g. there must be market interest rates, commercial lending periods and principal and interest repayment arrangements).

We can assist you in restructuring your borrowing arrangements to minimise the risk that such income generated from the LRBA will be taxed at 47% as non-arm’s length income (NALI).

30 NOV 2016

Drastic superannuation changes from 1 July 2017

From 1 July 2017 drastic changes will occur to our superannuation system.

Some of the main changes include:

- A $1.6 million superannuation transfer balance cap (i.e. a member of a superannuation fund can only have $1.6 million of superannuation savings in the tax-free retirement phase);

- Lowering the concessional (tax deductible) contributions cap to $25,000 (regardless of age);

- An extra 15% tax on concessional contributions made by individuals earning $250,000 or more a year;

- Lowering the annual non-concessional contributions cap to $100,000 per year (currently $180,000 per year); and

- All but abolishing the use of TRIS (transition to retirement income streams).

- Because we have about 7 months before the changes take effect on 1 July 2017, we look forward to working with you during this time to ensure that you are in a position to make an informed decision on how to manage your superannuation assets and implement tax effective and wealth creating strategies that may be applicable to your individual circumstances.

Please watch this space for more analysis on what the new changes will mean for you.

16 OCT 2016

Be aware of fraudulent SMSF schemes

The ATO and ASIC are concerned about various superannuation schemes such as:

- Dividend stripping schemes where franked dividends are not paid directly to shareholders, but rather to their SMSFs to strip profits tax-free from the company;

- Non-arm’s length limited recourse borrowing arrangements where the non-arm’s length provisions may apply to tax income generated from such assets at 47%. Note that if taxpayers put such arrangements on arm’s length terms by 31 January 2017, such income will not be taxed at 47% (but only at 15%).

- Schemes to divert personal services income where an individual performs services personally and payment for the services are made to a company or trust that distributes the income to the individual’s SMSF (so that the income will either be exempt for tax (if in pension phase) or at least concessionally taxed. Although you may not have been involved in such schemes, we are obliged to alert you in case you are ever contacted to enter into such schemes. After all, forewarned is forearmed!

5 OCT 2016

Restructure your limited recourse borrowing arrangements

If your SMSF has any related party non-commercial limited recourse borrowing arrangements (LRBA), you have until 31 January 2017 to ensure those borrowing arrangements are on arm’s length terms such as market interest rates, commercial lending periods and principal and interest repayment arrangements.

We can assist you in restructuring your borrowing arrangements to minimise the risk that such income generated from the LRBA will be taxed at 47% as non-arm’s length income (NALI).

12 SEP 2016

Change to budget super measures – the $500k cap is dead

The proposed $500,000 non-concessional contributions lifetime cap has been abandoned in favour of other limitations that are proposed to apply from 1 July 2017:

- if an individual’s superannuation balance is below $1.6 million, such an individual will be allowed to contribute up to $100,000 of non-concessional contributions per year (currently the annual non-concessional contributions cap is $180,000); and

- if an individual’s superannuation balance is $1.6 million or more, such an individual will no longer be allowed to make any non-concessional contributions.

The 3 year bring forward rule will continue to apply to individuals with superannuation balances below $1.6 million (i.e. individuals under the age of 65 can contribute 3 x $100,000 = $300,000 over a 3 year period).

The Government has announced the retention of the work test (i.e. individuals between 65 and 74 will only be allowed to make superannuation contributions if they are gainfully employed for at least 40 hours in a 30 day period in a financial year) and to postpone the start date of the proposal to allow catch-up concessional contributions for balances of less than $500,000, to 1 July 2018.

Please see our recent article for more information on how these proposed changes may affect you.

14 SEP 2016

Superannuation – First tranche of budget measures

The Government has released a draft Bill which, if enacted, will mean that from 1 July 2017:

- there will be no 10% rule - i.e. everyone up to age 75 (irrespective of whether the individual is an employee or contractor) will qualify for a tax deduction (subject to a $25,000 cap) when making personal superannuation contributions; and

- there will be no work test – i.e. everyone between 65 and 75 will be able to make a superannuation contribution without having to work.

We note that no more official information is available on the more contentious superannuation measures proposed (i.e. the $500,000 cap on non-concessional contributions and the $1.6 million pension limit) – we will keep you updated on any new developments on those issues.

31 AUG 2016

Superannuation – changes to collectables & personal use assets

Trustees of self-managed superannuation funds (SMSFs) are reminded that, from 1 July 2016, all collectables and personal use assets (e.g. artworks, jewellery and wine) will be subject to strict superannuation rules under the superannuation law. Transfers of such assets to related parties must be at market value, such assets may not be stored in the private home nor displayed in an office of any related party, and such assets must be insured in the name of the SMSF.

24 AUG 2016

Let us help you to find your lost super

According to the ATO, about $11.7 billion is sitting in lost super accounts (i.e. when the fund is unable to contact the individual and no contributions have been made to the fund for 5 years).

Please contact us if you think you may have some lost super so that we can assist you in tracking this lost super down. After all, this is your money which can be claimed by you at any time.

Don’t engage in dodgy retirement planning schemes

The ATO has warned against schemes where individuals who are close to retirement, channel dividends inappropriately through their self-managed superannuation fund for the main purpose of receiving franking credit refunds. The effect of such dividend stripping arrangements is to avoid paying franked dividends directly to a shareholder, but rather incorrectly to the shareholder’s SMSF.

Please contact us if you have been involved in such a scheme; the penalties for such tax avoidance schemes can be substantial (e.g. monetary penalties but also a sanction on your ability to continue to act as a trustee of your own SMSF).

17 AUG 2016

No exercise of ATO’s discretion to disregard excess concessional contributions

In the recent Administrative Appeals Tribunal (AAT) case of Re Azer and FCT, the AAT confirmed that no special circumstances existed under which the ATO could exercise its discretion to reduce an excess concessional contributions tax assessment to nil. The mere fact that the taxpayer was working multiple jobs and salary-sacrificing into different superannuation funds - and not keeping track of whether such contributions exceeded the then $25,000 limit - did not amount to special circumstances for the discretion to be exercised.

Please contact us if you have made multiple contributions to your superannuation or are unaware of the precise amount you have contributed this year so that we can assist you to manage your superannuation contribution caps. Leaving such planning until the end of the financial year is usually too late.

Risk of dying intestate or without a binding death benefit nomination

Upon the death of a person, the amount in that person’s member account in their superannuation fund must be dealt with. The amount could be used to fund a reversionary pension to a dependant, the amount might be paid as a superannuation death benefit to a dependant or be paid to the person’s legal personal representative (usually the executor of the estate). The person should complete a death benefit nomination which dictates how the person’s member’s account should be allocated.

In the recent Federal Court (FC) case of Ievers v Superannuation Complaints Tribunal, the deceased died intestate (without a will) and without making a binding death benefit nomination.

The FC confirmed that 100% of the superannuation death benefit (i.e. an amount of about $265,000) should be paid to the deceased’s de facto spouse (since the de facto spouse was the deceased’s sole dependant) and not to the LPR (and thus not into the deceased estate so other family members could not benefit).

To prevent such unforeseen circumstances, please contact us about your estate planning needs to ensure that your estate is distributed in accordance with your wishes.

10 AUG 2016

Windfalls from life events possibly exempt from $500k non-concessional superannuation contributions cap?

In a recent media interview, the Treasurer hinted that certain non-concessional contributions will not be subject to the proposed $500,000 non-concessional contributions cap announced in the recent 2016 Federal Budget. In particular, income from certain life events, such as a pay-out as a result of an accident, may be exempted from this cap.

The legislation introducing the Budget superannuation changes is expected to be introduced into Parliament after 30 August 2016. We will keep you informed as more details are announced.

In the meantime, please contact your Nexia adviser before embarking on any changes to your superannuation arrangements.